Why we fall for stock market charlatans

Financial Charlatan of the Year

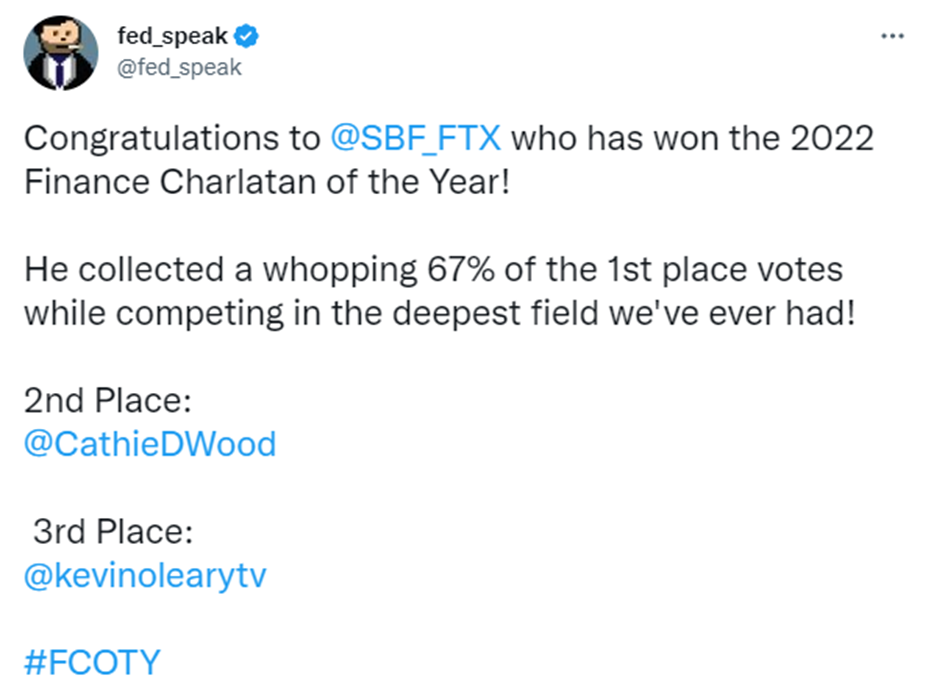

Every year, Twitter user fed_speak runs a popular competition called "Financial Charlatan of The Year". This tongue-in-cheek poll asks followers to nominate who they think has been the biggest charlatan in finance over the previous year. Naturally, the nominees tend to be people investors will have heard of, and past winners include Ross Gerber, Chamath Palihapitiya, and Raoul Pal. 2022's winner by a country mile was FTX founder Sam Bankman-Fried. ARK Invest's Cathie Wood took the second-place spot.

As you can see from the list of past winners, those who win the most FCOTY votes are not always people who have acted fraudulently. Instead, it can include investors with poor long-term performance track records but who present themselves as visionaries. Or investors who've encouraged investors into a stock market bubble. Often these enablers have drunk their own Coolaid; they have been true believers who have also lost their own money in these ventures too. (Although their copious management fees no doubt act as a salve to their pain.) However, that doesn't make them any less dangerous to investors' wealth.

As we enter a new year, investors' minds often turn to market predictions, tips or other advice. This means they will be particularly susceptible to the charms of the stock market charlatan. But why do we fall for them? Well, primarily, the charlatans are great salespeople. Consciously or subconsciously, they are particularly adept at knowing what influences investors and using those factors to convince them to go against their own best interests.

The Psychology of Influence

Some people are particularly prone to falling for sales patter. One such person was Professor Robert Cialdini, an academic psychology researcher at Arizona State University. Having realised that he consistently ended up being sold poor deals, Cialdini decided to study what influences people. However, he quickly realised the limitations of only doing research using university students in laboratory conditions. His genius was in realising that far more could be learnt from studying salespeople than students. So, to get greater insight into how it was done, he replied to advertisements for sales trainees, became a used-car salesman and ran parties for multi-level marketing products. In all cases, he took these organisations' training manuals together with his observations and analysed them to understand which actions were successful in generating compliance, as well as the psychological reasons why.

Overall, Cialdini found six main ways we are influenced: Reciprocity, Commitment and Consistency, Social Proof, Authority, Liking and Scarcity. He described them in his best-selling book Influence: The Psychology of Persuasion. The six influential psychological forces that Cialdini found are effective because they are generally good ways to make decisions or represent qualities we usually admire.

His aim was that by knowing how they are influenced would enable readers to defend against the power of these effects. For example, if we know that charities send out free pens with their literature because of our tendency to reciprocate a gift, we won't be tricked into donating. We may still decide to give to a good cause, but it won't be due to a misplaced desire to reciprocate apparent kindness.

Here are the kind of charlatans that the stock market investor is likely to encounter and how to avoid becoming one of their victims:

The Ramper

The Ramper only ever posts positively about the stocks they own. They often mention large addressable markets or come up with outlandish price targets. However, they never mention any risks or downsides and may become angry or aggressive with anyone who does. They may even create multiple account aliases, which then talk to each other, creating the impression of many interested parties. Then, when they sell out of a stock, they go quiet or sometimes even flip their view and immediately post negatively.

Why investors fall for rampers

Professor Cialdini found that when we are uncertain about something, we tend to look to what others are doing. This effect he called Social Proof. Most of the time, social proof is a good way of making a decision. For example, imagine you are on holiday in a small town looking for a place to eat dinner. As you enter the square in the town centre, you see two restaurants, one almost full and one mostly empty. Where would you choose to eat? Most of the time, the busy restaurant will be the better one. Since some locals will be in the know and choose the best restaurant, it will be busier. Social proof would be a good way of making this decision. However, it is certainly possible that the first people to enter the square that night randomly chose the now-busy restaurant and social proof led all the other diners to eat there, whatever the merits of the now-empty restaurant. (Note that restauranteurs know the power of social proof very well, which is why they always try to seat you in the window if you are the first to arrive!)

Social Proof is a powerful effect that the Ramper uses when they build up a picture of many excited investors enthusing about a stock. But, unfortunately, buying the most popular stock is rarely a good idea. As this study by Stockopedia Founder Ed Page-Croft found. Ed tracked the returns of the 100 most discussed stocks from popular UK investment discussion websites between 2014 and 2016 and found that these underperformed the UK All-share Index by over 18% during these two years.

How can investors avoid it

The first step investors can take is simply refusing to invest in any of the most popularly discussed stocks. However, as much as investors think they can be objective, it can be hard not to be caught up in the excitement of others. This is a largely unconscious bias. So while investors should be wary of muting others simply because they disagree with them, when it comes to the Rampers, as soon as they are identified, then muting and blocking them is always the best strategy.

The Tipster

The Tipster is someone who provides specific stock recommendations. Here, I don't mean everyone who provides a list of stocks they expect to perform well in 2023, such as the newspaper columns. (Although the wise investor should probably question whether they should make investment decisions based on the surface-level analysis of a 25-year-old journalism graduate who isn't allowed to invest in individual stocks!) I am talking about the paid services where a trader offers investors specific buy or sell advice or where investors have to pay for special access to see trades or discuss stocks.

One of the warning signs is when a Tipster only quotes their positive picks or trades. It is very easy to hold 50 stocks and only mention the five that have multi-bagged, even though they may have been tiny positions, and the overall performance at the portfolio level was terrible.

Why investors fall for tipsters

Nobel-prize-winning economist Daniel Kahneman showed that people are cognitive misers – our brains tend to seek solutions to problems that require the least mental effort. This means that investors are often tempted to take shortcuts and seek the opinion of others rather than make their own minds up. By seeking out the Tipster, we want the answer (the identity of the winning stock) without being willing to frame and carefully think through the problem (do the detailed stock research).

How can investors avoid it

Although all investors are likely to be cognitive misers at times, they are likely to know when we are taking a shortcut. This is the finding of a research paper by researchers Wim De Neys and his colleagues from the National Centre for Scientific Research (CNRS) in France. So when investors know that they want the results without doing the work, they should stop and recognise that this rarely works out well.

When it comes to investing services, perhaps the single most crucial question to ask when faced with these services is, "if this really worked, why are they offering it to you for a fee?". Take, for example, well-known trader Mark Minervini. He claims to have generated compound returns of over 20% for 37 years. However, some simple maths shows that if this was true and he started with, say, $100k, he would now have over $85m. Even if we account for him taking off living expenses over the years, he should still be a wealthy man. Too wealthy to be still running trading training courses for $5k at a time, perhaps?

The Stock Expert

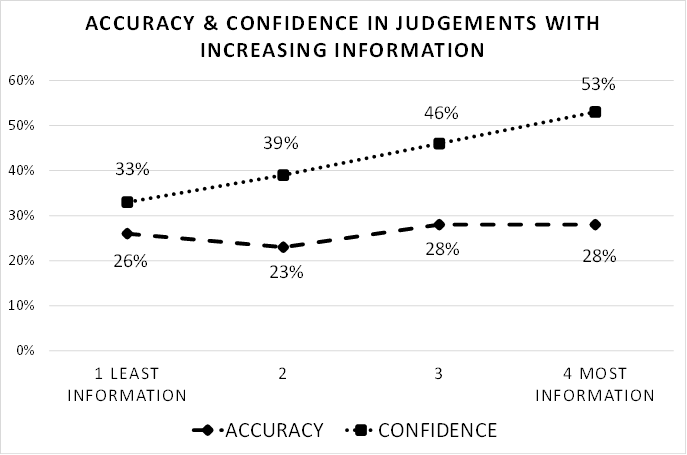

It is perhaps a little harsh calling those who know a particular company very well charlatans. Most are well-meaning and honest people. I probably have even been the "ackchyually" guy from time to time – the investor who knows almost everything there is to know about a company and always has an answer to any critique of the stock. The problem is that such an expert is likely to be the least-calibrated person when it comes to forming an accurate view of the company rather than the most. It comes down to the effect I have described before, where increasing knowledge is far more likely to lead to increased confidence than improved accuracy. This effect has been studied many times, and the results always look the same:

Increased information does little to improve accuracy but a lot to improve confidence, leaving the detailed stock researcher increasingly overconfident.

Why investors fall for stock experts

In his book, Cialdini describes the Authority effect. People tend to follow the lead of credible, knowledgeable experts. For example, physiotherapists can persuade more patients to perform the recommended exercises if they display their medical certificates on the walls of their treatment rooms. A uniform, or even just a hi-vis jacket, can mean that a request from the wearer is often obeyed unquestioningly. The authority with which the stock expert can answer any concerns in incredible detail acts as the same barrier to pertinent questioning.

How can investors avoid it

Investors should therefore be very wary of anyone whose argument is that they should be listened to purely because of their expertise. For example, someone who bats away genuine concerns about a tech company because they are an "expert in technology stocks" is likely to give poor advice. This can apply to third-party appeals to authority, too. As soon as the reason for holding a stock is given as "other well-known investors hold", the scene is set for a tragedy.

Investors should also take steps to avoid being the "ackchyually" stock expert themselves. High-quality and detailed research is the bedrock of the successful stock picker. However, if an investor won't listen to contrary views or starts to rely on their authority to shut down debate, they are on a slippery slope.

The Stock Promoter

My final stock market charlatan comes from the stable of company management. The stock promoter is a serial lister of companies. While a company's share price may see a brief period of buoyancy, the economics of the business always catch up with the stock price eventually. Such companies are often launched based on the latest investment fad and quickly pivot to what is trendy at the time. For example, an energy stock becomes a rare earth element miner before pivoting to blockchain and then back to energy. These kinds of companies always have a good story to tell.

Why investors fall for stock promoters

One of the reasons we find stories so engaging is that our brains are hard-wired to respond to narratives. Stories engage many parts of our brain, leading us to enjoy the experience far more than listening to facts and figures. The feeling of empathy that stories can cause the neurochemical oxytocin to be released, and oxytocin signals to the brain that 'it's safe to approach others'. The consequence of an oxytocin release is that you are more likely to trust the situation and the storyteller. Emotional events also cause the hormone dopamine to be released, which aids memory function and increases your enjoyment of the story. It is easy to see how these brain chemicals could lead us to unduly trust a Stock Promoter.

How can investors avoid it

The Stockopedia StockReport is a powerful tool in combatting this effect since it enables investors to see at a glance the financials of a company and how the Stockopedia algorithms rate it. Since I know I am a sucker for a good story, when I attend investor events, I check out the Stockreport for presenting companies ahead of time. I won't attend the management presentation if I don't like what I see.

I may miss out on the occasional good opportunity that isn't yet reflected in the numbers. However, on many occasions, this has saved me from being led astray by promotional management with a good story to tell and little else behind it.

Investors can never fully inoculate themselves from the lures of the charlatan; the biases that they exploit are always part of us. However, as Professor Cialdini found, being forewarned is being forearmed. By knowing how they are likely to be led astray, investors can be equipped to avoid the stock market charlatan when they appear in 2023.

About Mark Simpson

Value Investor

Author of Excellent Investing: How to Build a Winning Portfolio. A practical guide for investors who are looking to elevate their investment performance to the next level. Learn how to play to your strengths, overcome your weaknesses and build an optimal portfolio.

Disclaimer - This is not financial advice. Our content is intended to be used and must be used for information and education purposes only. Please read our disclaimer and terms and conditions to understand our obligations.

The book is referenced multiple times in Charlie Munger's Psychology of Human Misjudgement talk.

As for research, being an expert economist my view is stupid amounts of research has diminishing utility (or is that self justification for laziness)

Ahactually, Mark Rampson, is your top pick for 2023 Capital (LON:CAPD)

Obviously joking, know you're not a ramper (if you are you need to get better at it!).

It's crazy but even someone as obnoxious as me still wants social proof - not following people per SE but when someone holds something that I loke ideally after I have bought it, warm fuzzy feelings galore.

Great read - happy new year

Part of Cialdini’s large book-buying audience came because, like me, it wanted to learn how to become less often tricked by salesmen and circumstances. However, as an outcome not sought by Cialdini, who is a profoundly ethical man, a huge number of his books were bought by salesmen who wanted to learn how to become more effective in misleading customers.

Well, I bought it and read it for the former reason, but also used some techniques when I assumed the technical sales and support role towards the end of my employment. It was certainly never used to mislead customers though!! Certain aspects can be used to quickly generate a rapport when only communicating by email, which I found very important in building a relationship. The most important of which is replying to emails in a timely manner; so simple, but you'd be amazed how few of our competitors bothered to reply same day, let alone within an hour or two with detailed responses to all enquiries.

All the best, Si

I gave up on stock pickers years ago.

So called experts often have widely differing target prices for stocks, so that's not a good start.

I stopped reading bulletin boards too as most of them want to get rich quick talking up shares, and I have lost many thousands doing it

Now I read accounts, make sure they are solvent, consistently pay dividends, consistent growth etc.

A good share should sell itself, it shouldn't need too much promotion

I now make a little money instead of losing quite a bit

If he had started with 5k dollars, not 100k, then Minervini would have made 4 million, not 85 million, so the starting figure makes all the difference. Given what I know of his trading ideas, I don't doubt he has made millions from his trading. The fact that he is selling a training service need not be mutually exclusive to being a multi-millionare either. He says in his books that he believes in "giving back", which is why he wrote his books, and for 5k I wouldn't mind joining his course - I've already saved much more just on his chapters on risk management alone He may be many things, but Charlatan is not one them in my humble opinion. However, I don't think he could have made anywhere close to what he made, trading anywhere except the US markets. That's why I'm expanding my trading to US shores.

Mark Minervini net worth of $30m - not too shabby! I have enjoyed one of his trading books particularly. It has really helped me time my entry and exits. And also use his methods as a way to identify shares likely to do well in combination with stocko ratings and stock screens. Not my place to tell others how to approach investing, but reading his book been a real catalyst for improved returns - assuming that the stock market is flat or better.

Very true. Implementing stop losses and abiding by them was the turning point from what I read.

I can think of one particular commenter in the Telegraph comments section who fits several of the descriptions above and has cost me a few bob (due to my own gullibility).

I reckon Mark Minervini is driven by a big ego, but I don't believe he's a charlatan. I learnt from him and from one of his influences -- Jesse Livermore -- to deal with losing positions quickly. Even dyed-in-the-wool long-term investor Lord John Lee now reckons he often cuts losses at 20%. Focusing on the downside has been particularly handy for me over the past three years or so. FWIW, I reckon his need for purpose in his life drives his desire to teach others now (what would you do with your life if you'd turned about $30k into $30m and trading was all you knew?) And perhaps the high entry cost of his service forces a committment from others and helps to weed out time-wasters. Nevertheless, despite giving Minervini the benefit of the doubt, I'm receptive to hard evidence that he's a scammer. Does anyone have any?

I reckon his need for purpose in his life drives his desire to teach others now (what would you do with your life if you'd turned about $30k into $30m and trading was all you knew?) And perhaps the high entry cost of his service forces a committment from others and helps to weed out time-wasters. Nevertheless, despite giving Minervini the benefit of the doubt, I'm receptive to hard evidence that he's a scammer. Does anyone have any?

Well, I'm always reminded of that very embarrassing CNBC interview he gave in Oct 2021, where he was asked by the host what a company called Upstart, that he had bought only 4 days before, did in terms of its business. And he didn't know, so he pretended there was an audio problem and the line was breaking up in order to end the interview to spare his blushes. In that interview he claimed it was a great company and it (unsurprisingly for a relatively small company) had gone up 25%in 4 days since he bought. Hmmmm.... So you could make a case for him pumping it to his "believers". At the time the Upstart (UPST) share price was $392 and now it's $14.

And he does use influence techniques. Clearly by selling books and appearing on TV he has been able to set himself up as an "Authority". It's clear some here have fallen for that. Did Mark Minervini really invent risk management or stop losses? Of course not, these techniques have been around since before he was born! And the idea that he only writes books to "give back" is ridiculous... that's just a sales technique using the power of "Reciprocation".

Is he a "charlatan"? Probably. If it quacks like a duck and walks like a duck...

Interview here: https://www.mediaite.com/news/...

All the best, Si

The most interesting part of the Minervini Upstart interview is actually his inability to take a loss. Here's what I said about it at the time on SCL:

We’ve all been there, caught out by a bad position. And as a trader, Minervini should have known what to do: take the loss. Indeed, Minervini tweets regularly about the importance of stop losses. If he’d simply said [about what Upstart does], “I don’t know, but as a trader, I don’t need to know to make money”, then that would have been it.

However, Minervini’s loss aversion kicked in, and he appeared to fake technical problems to avoid the question, which opened him up to the internet’s ridicule. And then to further questions such as, if his trading record was as good as he claimed, why would he still be trying to sell trading services to the general public, or why he appeared to be still using a stock photo taken decades ago?

At this point, Minervini had another decision to make. If he’d simply laughed it off, then that would have been it. However, again, his loss aversion kicked in, and in order to “take on the trolls”, he began a series of tweets that gave the appearance of a man having a major mid-life crisis. The moral of the story is, when things go wrong, always take the first loss.

I've got an even scarier story of a man failing to take a loss, and it leading to disaster here:

Loss aversion is as ubiquitous as it is dangerous.

The 'problem' with minervini being a charlatan is that his methods work. None of his advice is bad, and he makes clear that he learnt the methods from others, regularly citing bill O'Neil and jesse Livermore amongst others.

I've no doubt that he's a capable trader, but I suspect trading is very mich a secondary income to his books, seminars and memberships, which are very expensive.

Does that make him a charlatan? Not sure. I'd say yes if the methods were trash, but they're not - I'd say every trader / investor would benefit from reading his books.

'They must know something' can be insidious.

I have tried to obtain a Stockopedia front page lay-out without the SCVR column and photo in the middle. They say it cannot be done.

On the North American exchanges one can avoid the editorial comments but there it is price that carries heavy influence.

Charlie Munger also said

“If you're not willing to react with equanimity to a market price decline of 50% - ..., you are not fit to be a common shareholder and you deserve the mediocre result that you are going to get.”

When it happens one feels a fool and can fall victim to the authority of Mr Market and the influencers well described in this article.

Statistics are only part of it. We remain dependent on someone else buying the stock we hold. For that to happen investor sentiment has to change and charlatans such as Fed governors have something to do with it. Inflation was 'transitory' a year ago.

The problem with Minervini is you can't debate anything with him, if anyone questions anything he says or does, he just comes out with his stock reply of "how many millions have you made" or similar. I used to have a look at his twitter account but don't anymore.

His methods work in the US markets but doubt he would trade in the UK markets, spreads are too wide, costs too high, I found I was getting stopped out all the time.

What do readers think about people like Louis Navallier, Eric Fry and Jeff Brown (all US based). Are the services they sell worth the money?

*Past performance is no indicator of future performance. Performance returns are based on hypothetical scenarios and do not represent an actual investment.

This site cannot substitute for professional investment advice or independent factual verification. To use Stockopedia, you must accept our Terms of Use, Privacy and Disclaimer & FSG. All services are provided by Stockopedia Ltd, United Kingdom (company number 06367267). For Australian users: Stockopedia Ltd, ABN 39 757 874 670 is a Corporate Authorised Representative of Daylight Financial Group Pty Ltd ABN 77 633 984 773, AFSL 521404.

I think I first heard of Cialdini via Charlie Munger's essay on The Psychology of Human Misjudgement:

I immediately sent copies of Cialdini’s book to all my children. I also gave Cialdini a share of Berkshire stock [Class A] to thank him for what he had done for me and the public. Incidentally, the sale by Cialdini of hundreds of thousands of copies of a book about social psychology was a huge feat, considering that Cialdini didn’t claim that he was going to improve your sex life or make you any money.

And:

Part of Cialdini’s large book-buying audience came because, like me, it wanted to learn how to become less often tricked by salesmen and circumstances. However, as an outcome not sought by Cialdini, who is a profoundly ethical man, a huge number of his books were bought by salesmen who wanted to learn how to become more effective in misleading customers.

timarr