Why a checklist may be more important than ever in the uncertain months ahead

It has become hard to tell the difference between silly season and the realities of what Brexit (especially a ‘no-deal’ Brexit) might actually be. This week we’ve had eye-catching scare stories about stockpiling food and medicine and the prospect of motorways being turned into permanent lorry parks...

With less than eight months to go before the official leave date, the more clarity that emerges about Brexit the more mind-boggling the exercise seems. Far from an orderly process, it feels more like a political barroom brawl. And considering that there could be far reaching consequences for at least some UK shares, the uncertainty (and the hysteria) is likely to ratchet up considerably in the coming months. So how can you prepare?

The art of ignoring noise

The issue for stock market investors is that the outcome and consequences of Brexit are hard to predict. One assumes that fund managers up and down the land are modelling various outcomes and considering how they might position themselves accordingly. But for individual investors, this kind of forecasting is a difficult and very possibly futile exercise.

In the uncertain months ahead what might make more sense is to tune out the market noise altogether. In ‘The Little Book of Behavioral Finance’, the analyst James Montier insists that worrying about much of this stuff is a waste of time. He writes:

“It is far better to focus on what really matters, rather than succumbing to the siren call of Wall Street’s many noise peddlers. We would be far better off analyzing the five things we really need to know about an investment, rather than trying to know absolutely everything concerned with the investment.”

A good example of how this works in practice can be seen in the checklist-approach used by Keith Ashworth-Lord, who I interviewed a couple of summers ago. He runs the Sanford DeLand UK Buffettology Fund, which over the past five years has achieved an impressive cumulative return of 128.7%.

As the name suggests, Ashworth-Lord’s fund is inspired by the US investing legend Warren Buffett. But more precisely, his modus operandi is based on something called Business Process Investing. Simply put, he has a strict checklist that each stock has to pass if it’s to make it into his fund:

Their business model is easily to understand;

They produce transparent financial statements;

They demonstrate consistent operational performance with earnings being relatively predictable;

They generate high returns on capital employed;

They convert a high proportion of accounting earnings into free cash;

Their balance sheet is strong without unduly high financial leverage;

Their management is focused on delivering shareholder value and is candid with the owners of the business;

Their growth strategy is more likely to rely on organic initiatives than frenetic acquisition activity.

Source: Sanford DeLand Asset Management

This is a useful list of criteria for anyone looking for high quality, Buffett-like businesses. But Ashworth-Lord also spends time digging through accounts and doing valuation work so he can buy the stocks he likes at prices below their economic worth. As a result, he thrives when markets are volatile. Because instead of being unsettled by market noise (like many others), his decisions are pre-made according to his checklist.

Ashworth-Lord is a buyer in uncertain conditions, when valuations fall and he can snap up shares of firms he knows well. And once he’s bought them, he holds them until the investment case changes. His checklist approach is a useful template for individual investors facing a particularly uncertain near future.

It would be remiss to not take a look at the kind of shares an Ashworth-Lord type strategy might consider at the moment. In recent years his fund has done well from positions in stocks like Games Workshop, Ab Dynamics and Bioventix among several other fast-growing small-caps.

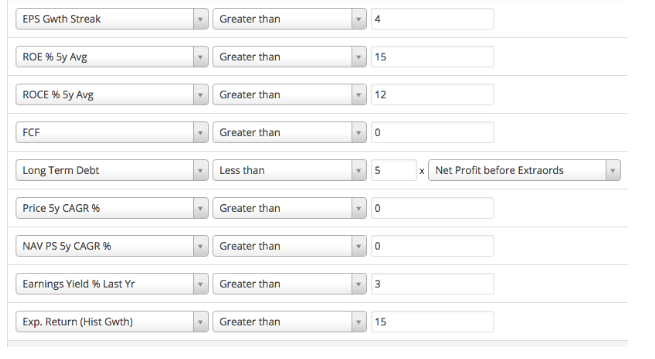

At Stockopedia we model various strategies that echo this kind of high quality, Buffett-like approach. This screen looks for firms with strong profitability and cash flow, low leverage, price strength and reasonable valuations.

This snapshot of the results (sorted by ROCE) include a set of stocks that may well be familiar to investors who look for high quality, high momentum stocks - although some have seen their prices weaken in recent months.

Name | Mkt Cap £m | EPS Growth Streak | ROCE % 5y Avg | Free Cash Flow | Earnings Yield % Last Year |

4,412 | 9 | 2,132 | 157.1 | 4.05 | |

342.9 | 6 | 72.8 | 14.2 | 4.40 | |

567.3 | 6 | 57.8 | 25.7 | 5.64 | |

2,924 | 8 | 43.2 | 139.2 | 8.65 | |

252.8 | 5 | 33.1 | 16.2 | 9.06 | |

4,554 | 5 | 29.9 | 152.2 | 6.87 | |

982.7 | 9 | 29.2 | 7.32 | 6.46 | |

2,005 | 5 | 26.4 | 225.3 | 11.4 | |

565.1 | 5 | 24.3 | 25.0 | 7.85 | |

451.4 | 8 | 23.9 | 25.8 | 4.88 |

A checklist to combat uncertainty

One certainty amid the months of confusion that lie ahead is that stock markets could become unsettled as the UK edges towards the EU door. The lack of clarity about what a deal (if there is a deal) will look like, sadly adds to the uncertainty. It’s in these conditions that it’s worth revisiting a personal investing checklist. Regardless of what strategy you use, preparing for the prospect of a bumpy road ahead could be time well spent. Ignoring the noise and focusing on what really matters could help you keep your head when everyone else is losing theirs.

If you enjoyed article, please spare a few minutes to vote for Stockopedia in the Best Investment Software Programme (Category 15) and Best Investor Education (Category 17) at the Shares Awards. Nominations are now open and we would really appreciate your vote! You can Vote Here

About Ben Hobson

Stockopedia writer, editor, researcher and interviewer!

Disclaimer - This is not financial advice. Our content is intended to be used and must be used for information and education purposes only. Please read our disclaimer and terms and conditions to understand our obligations.

At the risk of sounding like a mutual admiration club, Ben Hobson is one of perhaps half a dozen folk who 'got me' in the years I have been running this fund. What I would say is that the event of Brexit will look like a blip on the long-term road map of great companies five or ten years hence. And 10 years down the line the UK economy and businesses in general (especially great ones) will have been better off with a 'Hard Brexit' than the fudge concocted at Chequers by the hapless Mrs May and her svengali Olly Robbins.

Thanks Ben a very interesting article. I know many people are not in favour of this but I would always put a sector "reality check" on any screen results. Taking Jupiter Fund Management (LON:JUP) for example, the asset management sector is fairly low quality, in my view, because people and assets can walk out the door. The financials always look great for fund managers because they are not capital intensive. However, things can still go downhill pretty quickly.

It might also be worth looking back say 20 years at the ROCE i.e. through the cycle. My understanding is that ROCE is a "flow measure." So a recently robust figure could be because of a weak figure during a downturn. I'd be happy to be corrected if that is not the case.

So if a homebuilder has £100m equity and no debt and then makes losses of £15m for 3 years the equity falls to £55m. If we assume the homebuilder previously made profit before tax of £10m then its ROCE would be 10% before the downturn. After the downturn the ROCE would increase to almost 20% due to the fall in equity.

I think this is why Terry Smith always focuses on the average ROCE a company generates over a cycle (downturn and stronger periods). I don't think this really impacts any of the stocks on your screen though as far as I can tell. The stocks generally appear to be high quality. Probably just something to bear in mind.

I think of the analogy of a fund manger with fantastic returns in the last 3 years. If this is because they wiped out 80% of their equity in the prior 3 years then it isn't very impressive i.e. it is just a rebound. If the fantastic returns are representative of their long-term average returns then it is very impressive.

So we can think of a company's ROCE in this way. It is the through the cycle average ROCE that is important. Cyclical companies have very high ROCE's in good times (i.e. home builders) which are not representative of their long-term ROCE's. Some home builders reported great ROCE's on the rebound from 2008/2009 precisely because they wrote off much of their equity by writing down the value of land on their books.

That effect has largely played out now but the current high ROCE's of UK homebuilders doesn't necessarily make them attractive. It isn't likely to be representative of the long-term outlook for their ROCE's given that they are cyclical businesses. So ROCE filters often bring up fairly poor rebound companies. Your five year ROCE average filter appears to have meant that no low quality ones have come up in your screen.

I think this is something that Terry Smith has done very well to focus on i.e. not companies that look good today but companies that look good through the cycle.

BTW great to have Keith Ashworth-Lord comment here as I assume he is the comment above this one. A very interesting book - Invest in the Best. What is amazing is that the "Business Perspective Investing" should appear radical and unconventional. I.e. investing in terms of the underlying business rather than the forecasts etc.

In the long-term it is the business that delivers results and not the forecasts. Forecasts are just numbers on a page. People invest so much time making forecasts (will this year's earnings be higher and better than expected etc) rather than looking at the business.

As at the time of the referendum result, the nailed on inevitable upcoming hysteria, particularly from the Remain spectrum of the political divide, will provide huge opportunity for those with more stable heads which will typically come from the Brexit end of the spectrum simply because they don't fear the long run consequences of Leaving.

I quite agree with Ben that we should be drawing up such lists. Yesterday's one quarter of one percent interest raise caused a shudder in the markets. The USA is also tightening and Donald is playing trade wars, so it's not just Brexit that could cause a market correction. As for 'project fear' a friend of mine at a ratings agency points out that a nation typically does 60% of its trade with adjacent countries. Ignoring the the disruption to supply chains, does anyone really believe that you can substitute Australia and Canada for France and Germany?

Too many leaders such as the Governor of the BoE and many captains of industry are expressing real and serious concerns - this isn't 'project fear' it's now becoming 'project fact'.

Good article. Post reading Atul Gawande's "checklist manifesto" a couple years back, having a checklist has played a key role in my investment process. Helps to reduce errors/biases & enforce discipline.

Some of the commentary here directly or indirectly highlights Stockopedias main weakness - the fact that there are only three screening metrics that use 10 years data. It's been said before but I urge Ed and the team to provide at least 10 year averages particular for profitability measures.

Is Ben suggesting a checklist, similar to a pilots clipboard, checking instruments etc, before even firing up the planes engines? I certainly hope he is, I attended a Robbie Burns seminar back in 2009, where he gave out an example of such a checklist. I still use it today, although having photo copied the master several hundred times, it’s a little faded

*Past performance is no indicator of future performance. Performance returns are based on hypothetical scenarios and do not represent an actual investment.

This site cannot substitute for professional investment advice or independent factual verification. To use Stockopedia, you must accept our Terms of Use, Privacy and Disclaimer & FSG. All services are provided by Stockopedia Ltd, United Kingdom (company number 06367267). For Australian users: Stockopedia Ltd, ABN 39 757 874 670 is a Corporate Authorised Representative of Daylight Financial Group Pty Ltd ABN 77 633 984 773, AFSL 521404.

Ben,

I think you are dead right to point out the importance of a sensible checklist investing in uncertain times. Quality companies will continue to EPS out-perform irrespective of (EC) market noise. Mine simplified are:

Great time to top up if/when a correction occurs. It's time to be at least 20% in cash. Ian