Turnarounds - How to find value shares that are bouncing back

Back in 2012, shares in the media company Trinity Mirror looked surprisingly cheap given the amount of cash the business was throwing off. Despite its outdated business model, the newspaper publisher was still managing to juggle a high level of debt and a troublesome pension deficit. But what was more concerning was its seeming inability to adapt to a digital age. Investors were nervous about how long the cash would keep flowing. On top of that, there were worries that it would get sucked into the industry’s phone-hacking scandal and end up facing stiff penalties or worse. Only those with a cast iron constitution were prepared to buy the shares. Many believed it was a value trap, even at such an apparently cheap price.

But despite the negative sentiment, shares in Trinity Mirror took off and it became a multi-bagger over the next two years. Opinions are still divided on whether it’s a business with a sustainable future. But what isn’t in doubt is that Trinity Mirror was a classic Turnaround play. It was in a class of shares that rebound in price from what can sometimes look like terminal decline.

In the Stockopedia taxonomy of stock market winners, Turnarounds are the stocks that are both attractively valued and have strengthening price and earnings momentum. Value & Momentum have an intriguing relationship because as powerful individual factors that drive returns, they tend to work well at different times. Value has been shown to work best over long periods, but is particularly potent when markets are in recovery mode. By contrast, Momentum is much more time-limited and works most effectively during bullish, trending phases. For these reasons, the two factors are often used together to ‘smooth’ returns in portfolios over time. But when you get both value and momentum working together simultaneously in a single stock, it can be a great sign of a turnaround in progress.

The profile of a Turnaround

To understand the nature of Turnarounds, it’s useful to put them in context. In previous articles we’ve looked at how using Value as a factor on its own can lead to an uncomfortable exposure to shares that that might keep falling in price. With no other redeeming features, a stock that’s just cheap can end up being a dreaded Value Trap.

By comparison, stocks with an attractive valuation and good quality (but weak price strength) have the profile of Contrarian shares. These are the shares that may have hit temporary setbacks or are momentarily out of favour. But their high quality makes them statistically more likely to recover.

The third member of this Value ‘triumvirate’ are Turnarounds. They may not have the moat-like business strength or financial quality of Contrarians, but they may have turned the corner to recovery. While still cheap, brokers may start forecasting an improvement in fundamentals ahead of the reality, ratcheting up their earnings forecasts and kicking off a new share price trend.

One of the best authorities on Turnarounds is Peter Lynch, the one-time star fund manager at Fidelity Investments. In his book One Up on Wall Street, he paints a picture of them being stricken businesses, but insists that shares in successful Turnarounds can recover quickly:

“Turnaround candidates have been battered, depressed and often can barely drag themselves into Chapter 11 [bankruptcy]. These aren’t slow growers; these are no growers. These aren’t cyclicals that rebound; these are potential fatalities…”

In addition, Lynch reckons that there are several types of turnarounds:

- The bail-us-out-or-else

- The who-would-have-thunk-it

- The little-problem-we-didn’t-anticipate

- The perfectly-good-company-inside-a-bankrupt-company

- The restructuring-to-maximise-shareholder-value

Interestingly, the obvious candidates for Lynch’s first category - bail-us-out-or-else - are UK banks. Shares in the likes of RBS and Lloyds crashed ahead of their bail-out in 2008. But it remains to been seen when or whether investors who ventured back into those shares in the subsequent years will be repaid. By contrast, the share action at Trinity Mirror - swinging from 550p to 25p and back as high as 229p in seven years - echoes the sentiment of Lynch’s second category: who-would-have-thunk-it ?

As for the others? The Macondo oil disaster trashed shares in oil giant BP in 2010, and captures what Lynch mildly understates as the little-problem-we-didn’t-anticipate. Meanwhile, Harriet Green navigated travel group Thomas Cook away from imminent disaster in 2013 in an episode that you could lever into his perfectly-good-company-inside-a-bankrupt-company. And finally, restructuring-to-maximise-shareholder-value is perhaps amply reflected in any number of mining stocks that have come under huge pressure to shore up their balance sheets in the face of weak commodity prices.

Trending value

From a historical perspective, the argument in favour of blending Value and Momentum has probably been best put by US fund manager, James O’Shaughnessy. He’s spent many years - and devised several strategies - based on statistical patterns that emerge from the vast S&P Compustat database. He’s documented these findings in various editions of his book What Works on Wall Street. More recently he has shown how looking for stocks that look cheap against a combination, or composite, of several value ratios, together with improving price strength, is the basis for “the best performing strategy since 1963”. O’Shaughnessy calls this Trending Value.

But O’Shaughnessy is by no means the only one to have wedded Value and Momentum to get stunning results. Strategies driven by academic research have been a major reason why this blend of factors is used by some of the most forward thinking fund managers in the world.

How the experts find Turnarounds

One influential figure in this debate is Josef Lakonishok. As a finance academic turned fund manager, he spent years studying investor behaviour and the drivers of long term market returns. He and his colleagues concluded that investors typically rely too much on the past to make predictions about the future, and frequently pay too high a price for the shares that they buy.

As a result, Lakonishok’s preferred tactic was to identify well-priced shares at the moment the market is starting to notice them. He found that whatever your definition of ‘cheap’ is, value stocks consistently outperform glamour stocks by wide margins. So he suggested using ratios like price-to-book, price-to-earnings, price-to-cash flow and price-to-sales to find shares that look cheap against their sector average. He also wanted to see 6-months of positive momentum and stocks that had beaten expectations or were having their earnings forecasts upgraded.

Another way of applying Momentum to a Value strategy is to think about ‘fundamental’ momentum. In other words, a track record of improving financial health. In 2000, Stanford accounting professor Joseph Piotroski showed a way of doing this with a nine-point accounting checklist called the ‘F-Score’. That checklist is now used by some big institutional investors as a measure of a company’s quality. But in his original work, Piotroski specifically used it as a means of finding potential Turnarounds among the cheapest stocks in the market. His studies found that those with the highest financial strength often went on to outperform - on average by 7.5% annually over a 20 year backtest.

Tracking the performance of Turnarounds

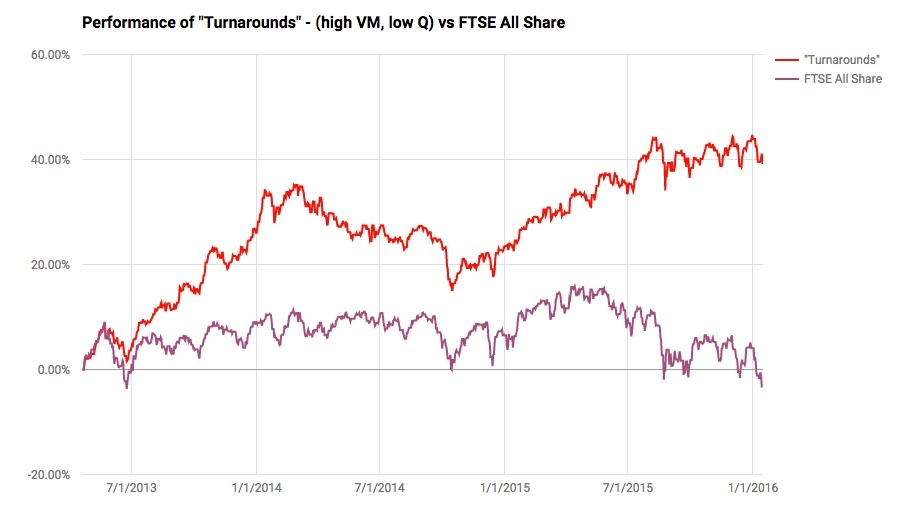

We can use the Stockopedia StockRanks to assess the performance of Value & Momentum shares over the last few years. The following chart was created using the Turnarounds Stock Screen to build a portfolio first selected in April 2013 and rebalanced annually in April. It simply searched for shares qualifying for the following criteria:

- Market Cap > £50m (i.e. no microcaps)

- Quality Rank < 60 (i.e. below average quality)

- VM Rank > 90 (i.e. attractively priced, high momentum)

Although this test covers a very limited timescale, it’s remarkable just how well the Turnaround approach has done over the period - returning around 40.0% against a muted FTSE All Share.

Where Turnarounds go next

One of the biggest areas of concern in the hunt for Turnaround plays is that the Momentum ebbs away. Value shares that are on the mend can be more susceptible than others to a sudden change of fortune that causes investors to run for the exit. In the absence of strong or improving quality signals, investors could be left holding a value stock that simply drifts if the momentum collapses.

It’s also worth noting that a Turnaround can take years to get going, but then unfold very quickly. Shares in greeting card distributor International Greetings collapsed from more than 400p to less than 20p through 2007 and 2008. While the price did rise in later years, it took until 2015 for the momentum to carry the price back through 100p and beyond.

Crucially, what International Greetings showed was how a typical Turnaround profile can quickly morph into that of a High Flyer (as Ed wrote about here). Smart investors like the fund manager Gervais Williams had cottoned onto the turnaround story early, but as its momentum accelerated and its financial strength improved in early 2015, International Greetings no longer looked obviously cheap. Instead, it carried the hallmarks of a high quality, high momentum share - which has been the classic profile of some of the UK’s best performing stocks.

Lessons from Turnarounds

To varying degrees, the combination of attractive valuation and positive price strength can be found in the strategies of some of the world’s best known and most successful investors. Academic research shows that it’s an effective way of spotting beaten down shares that might be recovering. And our brief analysis using the StockRanks shows that it has worked very effectively over the past three years.

But it’s undeniable that in the absence of business and financial quality, investing in Turnarounds can be risky and unpalatable. After all, the strategy means digging around among cheap shares that may have suffered major upsets and face unpredictable futures. But when they work successfully, they can reward investors with sudden and spectacular gains.

To find out more about the taxonomy of stock market winners, you can browse through the entire series:

- Towards a taxonomy of stock market winners

- Contrarian stocks - how going against the crowd can put you ahead

- High Flyers - how to beat the market in expensive and highly priced shares

- Turnarounds - how to find value shares that are bouncing back

- Falling Stars - how to handle glamour shares that fall from grace

- Value Traps - how to avoid bargain stocks that might never recover

- Momentum Traps - how to avoid the siren song of overhyped stocks

- Sucker Stocks - why do we love to own the worst prospects in the market?

About Ben Hobson

Stockopedia writer, editor, researcher and interviewer!

Disclaimer - This is not financial advice. Our content is intended to be used and must be used for information and education purposes only. Please read our disclaimer and terms and conditions to understand our obligations.

YEP STICK YOUR HEAD IN THE SAND AND SAY "NOTHING BAD IS GOING TO HAPPEN ! NOTHING BAD IS GOING TO HAPPEN ! " when you pull it out all that bad stuff will all be over; things will be back to normal.

I can see it working in a bull or trending market as per your chart. However we are in a bear market with FTSE down, S&P down, NIKKE down, and commodities prices are at their lowest, china has been battered everything points to a slowdown in the global economy. The HAPPY news doesn’t like to mention the C word but the down side risk of a crash will be at least 2000 points DOWN, turning most of these turnarounds into junk. Ah but let say I’m wrong, well the upside maybe about 600 points. This means Spectacular losses and mediocre gains.

Incidentally the last time this happened Lloyds, RBS el al. were turned into Zombies under government control. Many investors lost their shirt.

Yes, I still want to buy shares, partly because I want my savings to earn me dividends and in any case, any other method of preserving the buying value of my money is pathetic in comparison to inflation and/or ties up my money beyond reasonable usage. Whatever happens to the Footsie, the value of the pound, dollar, euro, oil or gold bullion, Brexit or no Brexit, I know that all us us will have to eat, run our cars and live somewhere. Life will continue, we will continue to work and use money daily. Businesses will continue.

As the fifth largest economy in the world, we are hardly destitute, whatever happens and it is deeply offensive for those of us who lived through the 1950s for soft, obese, over-affluent politicians to talk about "austerity". Not being quite as rich as we'd like in our greedy dreams is not poverty. There are poor people in this country but they exist because of our cult of the individual and inability to share the wealth with the less able to fight for it. Besides, the poor and under-privileged are significantly under-represented on the stockmarket. It is equally offensive for any of us to imagine the world we inhabit is remotely like that of the Great Depression. If things get tough, my grandchildren may be obliged to share an Xbox and surf on a single iMac, not go without shoes. We can buy strawberries every day of the year in all supermarkets.

Investing in substantial businesses is not like betting on horses. It's not all over in 6 furlongs and we laugh or scowl and rip up our slips. I own a chunk of the very same Carillon that is currently renovating the centre of Birmingham and after that will continue somewhere else. I am helping Interserve build a new and much needed multi-storey car park for the Leicester Royal Infirmary and I am proud of what Galliford Try did for Leicester Tigers stands. The moment we all drive fully electric cars, I'll sell my RDSB, assuming, of course that they haven't diversified into the new generation of batteries by then. Who'd bet they won't? Do they look stupid? I could go on.

Of course, if I had borrowed my investment money at 6% and expected to become a millionaire in a week or so without doing a stoke of actual work, I could be quite stressed by now. Why hadn't I used the money to buy scratch cards? I might have got lucky.

Today I received the latest missal from Roger Martin-Fagg, someone who spends a great deal of time analysing the economy. He wrote:-

"The Footsie is on a P/E of 16.7 compared to 15 long run average this implies an overvaluation of 7%. But if we take the cyclically adjusted P/E which averages company profits over 10 years (the cycle is typically seven years) it has averaged 20.8 since 1983. Today it is 14.9. This suggests the market is undervalued!

As 80% of Footsie profits are earned in dollars, a further weakening of sterling against the dollar will boost reported earnings and is another reason to suggest that rather than fall further, it will stabilise around 6000. The yield is 3.4% which is better than most if not all cash deposits.

Please note that the most frequently traded shares are traded by machines which are pre- programmed. This always causes a decline in price to gather momentum until a floor is reached, at which point the machine issues buy instructions and the momentum is upwards. The major stocks are not moving based on human assessment of risks andrealities. All the algorithms will be out of date, based on assumed, historic drivers of share prices. Hold tight; the markets will recover as quickly as they crash."

That last reference to the way prices move nowadays is probably the major reason we should not treat movements in the stockmarket as we would have 100 years ago or even 25 years ago. Mr Market is now a bot. I'm not.

Go to the Stockopedia home page.

Look chart on the right hand side which way is it trending ?

Look at the top 10 value, momentum, quality and growth stocks.

What colour is dominant (red or green) ?

What could those Algorithms in Sockopedia be saying to you ?

You sort of said it in your first statement. Its about real stuff ! stadiums being built or planes flying around, cars being driven, people using physical services. Well this stuff is in decline GLOBALLY ! We know this by commodity prices being low, the dry goods index( stuff being shipped around the world) being low, china. Its Not the about the ponzi scheme we call the economy.

You don't need a super computer with an advanced heuristic trading algorithm to tell you where this will end.

Buy, Sell or Hold, It fairly obvious !

Of course, in the short term he production of stuff will ebb and flow but the world's population continues to expand and people whose carbon footprint used to be tiny now want the said stuff. There are still people who exist on less than a dollar a day. They represent a huge proportion of the world's masses. China's major problems include industrial pollution and lack of potable water. The relative decline of the incredible boom once the political restraints were lifted by China and the collapse of the soviet union is, in my view, nothing but a reasonable correction of an unsustainable situation. Very few people vote for a reduction in their standard of living so it will continue to rise, inexorably until the human race completely wrecks the planet. That' sadly, is where it will end but, in what's left of my lifetime, we in the greedy West will continue to get richer and richer.

This TED talk puts the global economy and its relative significance into interesting perspective. Life is all about getting enough to eat and while what Tris Stuart says continues, the short term movement of prices of notional matters is just a temporary inconvenience. https://www.ted.com/talks/tristram_stuart_the_global_food_waste_scandal?language=en#t-171772

*Past performance is no indicator of future performance. Performance returns are based on hypothetical scenarios and do not represent an actual investment.

This site cannot substitute for professional investment advice or independent factual verification. To use Stockopedia, you must accept our Terms of Use, Privacy and Disclaimer & FSG. All services are provided by Stockopedia Ltd, United Kingdom (company number 06367267). For Australian users: Stockopedia Ltd, ABN 39 757 874 670 is a Corporate Authorised Representative of Daylight Financial Group Pty Ltd ABN 77 633 984 773, AFSL 521404.

Ben thanks for this article always on the look out for turnaround companies. A few points, Lloyds Banking (LON:LLOY) did go from 25p to over 70p so for some investors have been well rewarded. Re Piotroski F score I did find quite a few companies that high F scores but low Altman Z-Scores ie likely to go bankrupt, so I would suggest to check both scores.

Re International Greetings (LON:IGR) is that why they have fallen back lately because of recession fears? Seems like they are vulnerable to slow downs.