Three types of stocks to avoid in the current market

The current UK markets are brutal for companies that fail to meet expectations. Even short-term issues are punished severely. While it can be challenging to predict which companies will issue a profit warning next, some companies have seen very large declines, while others have escaped with a mere flesh wound. I am interested in what makes the difference and how investors can avoid the companies that are going to leave a gaping wound in their portfolio.

In August, I looked at some of the traits of the worst-performing stocks this year. This time, I am looking at the characteristics of the stocks that have performed worst in the recent past. To find out which they are, I used the Stockopedia screening tool to look for companies that have fallen more than 50% in the last month. I limited it to companies with a market cap above £5m, and therefore above £10m before their recent fall, to avoid companies where illiquidity may be driving the volatility, not trading performance. Here are the results of that screen:

From looking into these seven worst performers, I can identify three types of stocks that investors will want to avoid owning:

Expensive stocks with declining prospects

Stockopedia has a nice feature whereby past StockReports can be accessed at specific dates in PDF format:

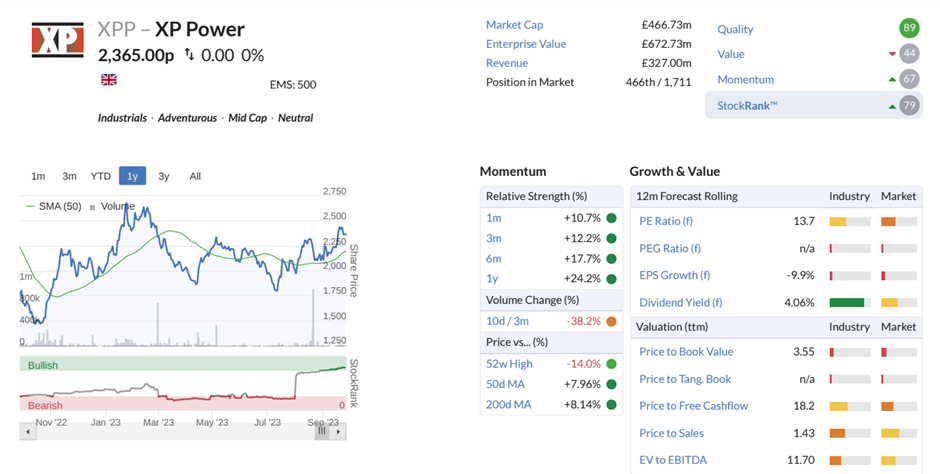

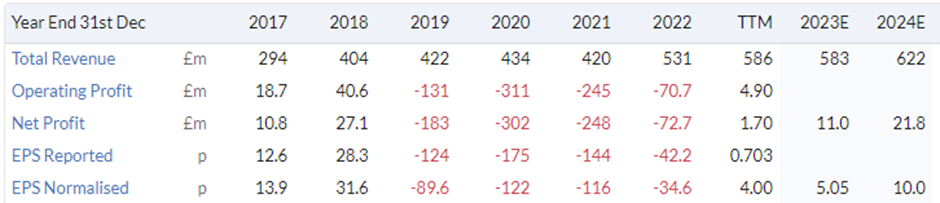

This enables investors to see what Stockreport looked like before a precipitous fall. In this case, XP Power (LON:XPP) :

The first thing that stands out is that this stock isn't particularly cheap, with an EV/EBITDA of 11.7. This seemed expensive for a stock where 2023 normalised EPS was forecast to be below what the company delivered in 2017:

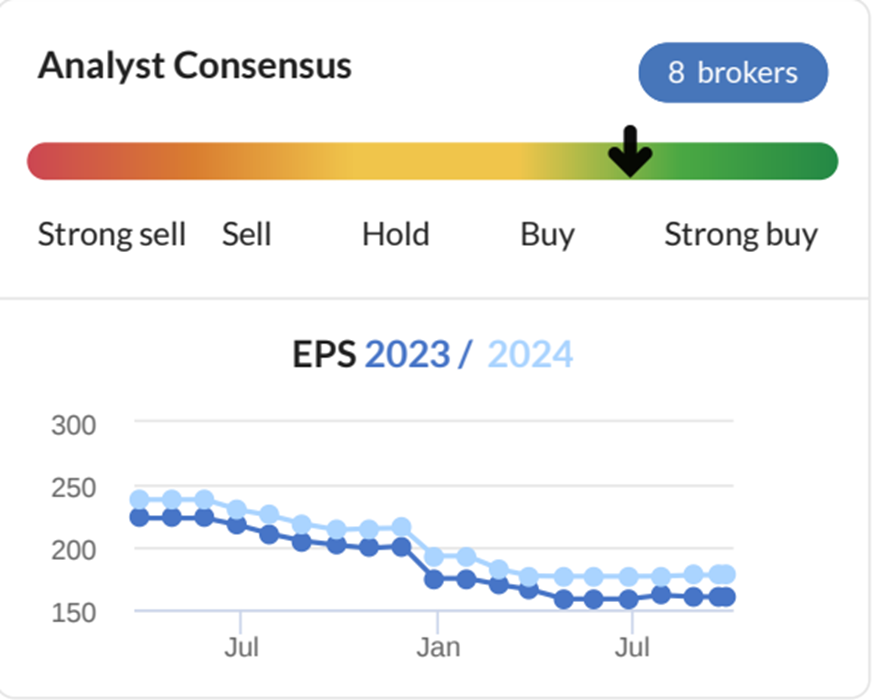

Part of the problem was that these analysts' forecasts had been consistently declining:

But even more concerning should have been the rise in net debt:

And in the trading update that caused this steep drop in share price, the company now said:

The Group continues to be in compliance with its banking covenants but is now expecting net debt / Adjusted EBITDA to be close to or above current covenant limits in the near-term. The Group is initiating dialogue with its lenders to seek covenant and liquidity flexibility through the year-end and into 2024. We are also exploring other near-term options to strengthen the balance sheet, to bring leverage back to within our target 1-2x net debt/Adjusted EBITDA range, restoring the flexibility necessary to allow the Group to take full advantage of the strong organic growth opportunities across the business.

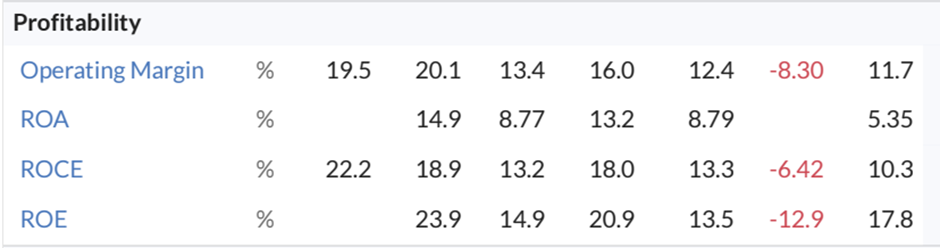

This suggests that there may be some kind of fundraise on the way. On top of this, they took the unusual step of cancelling a dividend already declared, with the shares marked ex-dividend. Many consider the company a high-quality growth stock. However, there is little evidence of that growth in normalised EPS, apart from two years of short-term positive trading, 2017 and 2022. The quality metrics have also been declining recently:

This mistake many investors appear to have made is assuming that the fall from 2021 highs meant that the stock was due a bounce. Indeed, after a dip in the Truss trough in 2022, the shares were being bid up despite the declining forecasts:

As some may have found out, to their cost, past glories say little about future returns.

For Metro Bank Holdings (LON:MTRO) , it would take a banking analyst to fully understand what went wrong here. My understanding is that Metro's strategy was to focus on growing high-quality customer deposits, which tend to be sticky. And so they proved. Despite well-publicised challenges, the bank has not seen significant deposit outflows, perhaps because three-quarters of deposits are under the FSCS limit. The issue appears to be where they have invested the money, including in a portfolio of commercial loans secured on immovable property (so-called CLIP Loans). Metro believed these loans were eligible for a 50% risk-weighting for the regulatory capital requirement, but it turned out to be 100%. After the error was discovered in 2019, Metro was fined for failing to maintain adequate internal controls and later fined again when management failed to report the error promptly. It had hoped regulators would have allowed them to use internal models rather than standardised ones to calculate regulatory capital, which was ultimately denied. This left the bank operating too close to their common equity tier 1 ratio for comfort, and they needed extra capital, which they have now raised at 30p, significantly diluting existing holders.

I will leave it to those more au fait with banking to judge whether there were specific warning signs for this month's fall. However, I will point out that their record of profitability was pretty patchy:

This is a period when banks such as Barclays (LON:BARC) , Natwest (LON:NWG) , and Lloyds Banking (LON:LLOY) were consistently profitable. Given that Barclays (LON:BARC) trades on 0.4xTBV, if you are into banks, why take the risk on Metro Bank Holdings (LON:MTRO) ?

Story Stocks

Our brains are hard-wired to respond to narratives. The empathy that stories elicit causes the neurochemical oxytocin to be released, and oxytocin gives a signal to the brain that 'it's safe to approach others'. The consequence of an oxytocin release is that you are more likely to trust the situation and the storyteller. Emotional events, even just imagining the profits you will make and how you will spend the money, will cause the hormone dopamine to be released, aiding memory function and increasing your enjoyment of the story.

This makes 'Story Stocks' dangerous for our wealth. Our love of a good story can lead us to buy into the type of stocks that are unlikely to generate a positive return. Stocks that are consistently loss-making, especially those with negligible revenue, must have a good story attached to them. Nobody puts up equity capital for an idea that sounds boring and unfeasible.

The problem is that no one is putting up fresh equity capital at the moment. So when things go wrong, there is little safety net for companies that don't currently generate free cash flow. This is what has happened to Horizonte Minerals (LON:HZM) recently. They are a pre-production miner that was meant to be fully funded through to production. However, on the 2nd of October, the Company announced:

…it has made good progress in completing the final detailed engineering and construction design for Line 1 of its 100%-owned Araguaia Nickel Project. This work, along with a comprehensive cost review, has resulted in changes to the design and execution scope, which are expected to increase the overall capital expenditure requirement by at least 35% (of current capex budget) and delay first production to Q3-2024.

Although the Company says it is:

… is working on a plan with its various financial institutions together with the cornerstone shareholders for a financing solution to complete construction.

A delay and budget increase of this size, so close to the original planned production date, has seriously undermined confidence in management. Any funding solution may be seriously dilutive to existing holders.

I am slightly harsh in describing Horizonte Minerals (LON:HZM) as a story stock. They appear to have a real mine, with real prospects to be in production. But that will be little salve for anyone who held the shares before these falls. In the current markets, investors may want to avoid any company that has zero revenue:

No matter how bright the future prospects may appear, companies without current revenue, profits, or cash flow are at the mercy of others if something goes wrong.

Renalytix (LON:RENX) may not be a zero-revenue company:

However, its sales are small compared to its current market cap. Prior to the recent fall, it was on 26 times sales:

The cause of the recent fall appears to be results that the Company disappointed on revenue. A growth rate of 15% isn't enough when the Company is on this sort of rating. Their operating loss in the year to the 30th of June was $42.4m compared to a revenue of $3.4m. Despite raising around $20m in February, they had just $24m gross cash on the 30th of June and just $13m net cash. It looks very much like they will need to raise fresh equity soon, at a very tough time to be coming to the market cap in hand.

Fads

Fads are companies whose products hit a wave of short-lived public buying, but investors make the mistake of valuing the current positive trend much too far into the future. Before too long, the fickle buying public has moved onto the next craze, leaving the Company with excess inventory and poor prospects. One such fad of recent years has been "fintech". Of the big fallers, two are described as being in this category:

REGTECH OPEN PROJECT (LON:RTOP) :

RegTech Open Project plc is an independent fintech company.

RC365 Holding (LON:RCGH) :

The Company, through its subsidiary, Regal Crown Technology Limited, is a fintech solutions service provider. Its business segments include Payment gateway solutions (online and offline), IT support and security services, CatchAR and Maid-maid Matching.

It seems that these companies are a little late to the party. The idea that "fintech" companies should be given eye-watering multiples peaked in 2021, together with their share prices. Many larger and more reputable companies, such as US giant Block, are now back to or below the levels they were trading at before the fintech bubble:

Another fad has been "Green Technology" companies. EQTEC (LON:EQT) appears to be in this space:

The Company uses its advanced gasification technology to generate safe, green energy from over 62 different kinds of feedstock, such as municipal, agricultural and industrial waste, biomass, and plastics.

Investors can make a lot of money buying into the latest fads early. After all, in a 2009 speech, legendary trader George Soros said:

When I see a bubble forming, I rush in to buy, adding fuel to the fire.

However, to avoid being left holding the bag, they need to know when the fad is peaking and get out quickly. If they don't have a good track record of calling these correctly, they should leave these fads well alone.

Conclusion

Not every company that meets one of these criteria will turn out to be a terrible investment. However, given the uncertainty over current trading for many companies, we can expect further profits warnings ahead for UK stocks. I am not sure I am clever enough to guess which companies will warn and which will prove resilient to current economic conditions. For example, I would have naively assumed that the 5G telecoms rollout would be a defensive tailwind for companies like Spirent Communications (LON:SPT) and Calnex Solutions (LON:CLX) , yet it has proven anything but defensive. (Calnex only just misses out on appearing on this screen, down 48% in the last month.) So, it seems a better strategy to avoid the type of stocks that are likely to be worst hit by any profits warning than try to predict which companies won't be affected by weak economic conditions or higher inflation. In the current market, investors would be best served by avoiding highly-priced companies with declining prospects or large debt, companies not fully funded to cash flow break even, or those involved in the latest market fad.

About Mark Simpson

Value Investor

Author of Excellent Investing: How to Build a Winning Portfolio. A practical guide for investors who are looking to elevate their investment performance to the next level. Learn how to play to your strengths, overcome your weaknesses and build an optimal portfolio.

Disclaimer - This is not financial advice. Our content is intended to be used and must be used for information and education purposes only. Please read our disclaimer and terms and conditions to understand our obligations.

great article - was expecting "debt" to be top of the list to avoid - but you sneaked it in with an honourable mention ref xpp. I used to hold xpp back in the day - it used to have minimal debt and great cashflow very surprised to see that the wheels have come off as bad as they have done. i sold at great profit but it still ended as a disaster as proceeds went into carnival plc (cruise company) about 2 weeks before covid turned up - plenty of ways to lose ones shirt in this investing game.

Hi Mark. Great article, my favourite of yours so far. Loved how you modelled the process through using XP Power (LON:XPP) data prior to the profit warning. It all seems so obvious in hindsight! I've been culling anything with big debt in my portfolio in recent months and paying a lot more attention to falling analyst eps expectations. The only company that I've held onto with these characteristics is Mobico (LON:MCG). Mainly because I'm convinced it going to make so much cash it won't matter, I'll most likely get burned with a profit warning and wish I'd listened to you! Cheers. Ben

*Past performance is no indicator of future performance. Performance returns are based on hypothetical scenarios and do not represent an actual investment.

This site cannot substitute for professional investment advice or independent factual verification. To use Stockopedia, you must accept our Terms of Use, Privacy and Disclaimer & FSG. All services are provided by Stockopedia Ltd, United Kingdom (company number 06367267). For Australian users: Stockopedia Ltd, ABN 39 757 874 670 is a Corporate Authorised Representative of Daylight Financial Group Pty Ltd ABN 77 633 984 773, AFSL 521404.

Very good article indeed.