Momentum Traps - how to avoid the siren song of overhyped stocks

Faced with choosing between a $10 bottle of wine and a $90 bottle of wine, which would you go for? In one experiment - with the prices of each wine clearly marked - nearly twice as many people preferred the taste of the most expensive bottle. But unknown to the volunteers, the two wines were exactly the same.

This test was carried out by American researchers investigating how pricing can influence the brain’s perception of how ‘pleasant’ something is. Told it’s expensive, we tend to like it all the more. It’s an example of what behavioral scientists say is a flaw in human emotions that causes us to be overly-influenced by a good story.

The read across for investors could hardly be more stark. Stories in the stock market are like a magnet. With herds of followers, these popular shares typically boast eye-catching price momentum. Yet a good proportion of them hide deteriorating fundamentals and stretched valuations that can be harder to spot (and, for some, easy to ignore). These are the market’s glamour stocks which may well be Momentum Traps - stocks where a sudden change in sentiment could see their momentum crash.

Of all the dangers that investors face, perhaps none is more seductive than the siren song of stories. Stories essentially govern the way we think. We will abandon evidence in favour of a good story - James Montier

Signs of a Momentum Trap

Small cap stocks soared through 2013, and by early the following year some valuations looked frothy. Swept up in a wave of bullish exuberance, popular ‘blue sky’ companies like Blur, Monitise and Cloudbuy were showing some of the classic signs of being momentum traps. As sentiment towards small caps drifted through the next 12 months, the price of each share was pummelled.

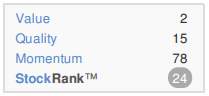

The common traits shared by these and other momentum traps was that their strong price momentum hadn’t been matched by improving fundamentals. Yet they looked expensive and their low QualityRanks pointed to firms that either weren’t profitable at all or were flagging as potentially distressed. Importantly, these were some of the most talked about small caps at the time, promoted by brokers and heavily traded by investors. They were the polar opposite of traditional ‘value’ shares but investors lapped them up all the same.

In The Little Book of Behavioural Investing, James Montier of investment firm GMO, says that one of the reasons why people shy away from value investing is that value shares tend to come with poor stories. As a result they end up being despised rather than admired. He explains: “Which would you rather own? Psychologically, we know you will feel attracted to the admired stocks. Yet the despised stocks are generally a far better investment. They significantly outperform the market as well as the admired stocks.”

Indeed, evidence that momentum stocks underperform dates back to a 1993 study by three researchers who made a personal fortune from their findings. Josef Lakonishok, Andrei Shleifer and Robert Vishny showed that investors consistently overestimate future growth rates of glamour stocks relative to value stocks. They said this was because investors typically make judgement errors and extrapolate too much of the past to make predictions about the future. They proved their point by going on to run billions of dollars in their own fund management firm called LSV.

Testing the performance of Momentum Traps

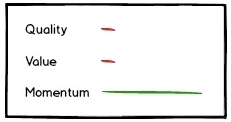

In Stockopedia’s taxonomy of stock market winners (and losers), Momentum Traps typically have StockRanks that reflect strong momentum but poor value and quality. We can build a screen for these stocks by setting the following filters:

- Momentum Rank > 80 (i.e. high Momentum)

- QV Rank < 40 (i.e. poor combined Quality and Value)

- Market Cap > 100 (i.e. to focus on the more well known shares)

- Top 25 stocks by Momentum Rank (i.e. 25 highest Momentum shares in the set)

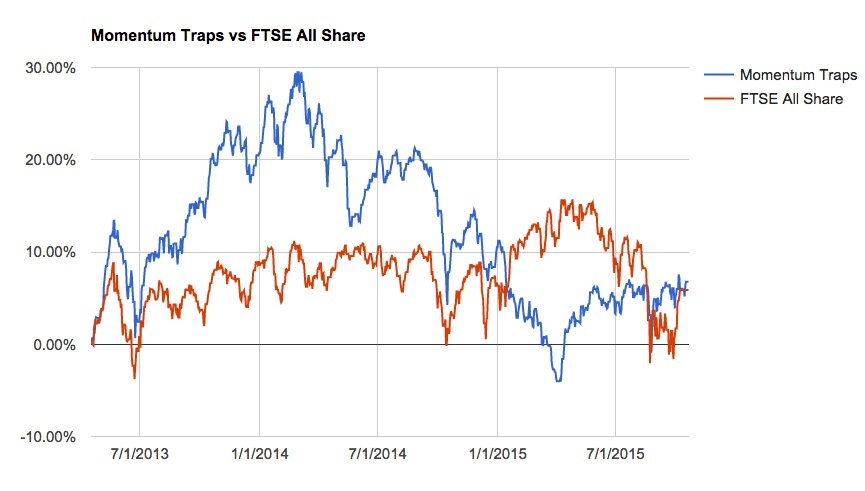

We’ve used the Stockopedia StockRank archives to generate the performance history of a 25 stock portfolio rebalanced annually since April 2013. The results are quite startling

What happens so often with Momentum Traps is that they outperform the market dramatically… but only for a while. This strong price performance lulls investors into a false sense of security and draws in the suckers right at the wrong time. Most investors buy these stocks at the top, and suffer terrible underperformance when gravity reasserts itself. As we can see the Momentum Trap portfolio has tracked the FTSE All Share over the last two and a half years but broken everyone’s hearts in the interim.

Through 2013, the Momentum Traps portfolio was very much an all-cap affair, with stocks ranging from 3i to Nanoco and Blinkx. There were (and continue to be) some stocks that held on to the momentum and did well. But in 2014, it was weighted much more heavily towards small caps. It’s here that the trouble starts. As sentiment cooled towards smaller stocks, those that were overstretched paid the heaviest price. Companies like eServGlobal, Quadrise Fuels, Johnston Press and a handful of resources shares have continued to slide.

Dodging a momentum trap bullet

Using the above rules on today’s data set, we’ve compiled a list below of stocks that could see their momentum turn if investor sentiment changes. The companies include some popular names like Hutchison China MediTech and Optimal Payments.

Note that the ‘buy’, ‘hold’ and ‘sell’ recommendations of the brokers that cover each company are broadly positive in their outlook. Detailed research may uncover nothing to worry about with these shares. However, QV Ranks of below 40 (out of 100) certainly warrants close attention and suggests things could be more precarious than the broker recommendations infer.

| Name | Momentum Rank | QV Rank | # Buy Recs | # Hold Recs | # Sell Recs |

| Harworth | 99 | 37 | - | 1 | - |

| Admiral | 98 | 25 | 1 | 10 | 2 |

| OneSavings Bank | 98 | 29 | - | 4 | - |

| Aldermore | 96 | 17 | 3 | 5 | - |

| Hutchison China MediTech | 96 | 14 | - | - | 1 |

| Optimal Payments | 95 | 29 | 4 | - | - |

| Grainger | 94 | 10 | 3 | 4 | - |

| Severn Trent | 94 | 25 | 2 | 9 | 1 |

| NMC Health | 93 | 20 | 6 | - | - |

| Dignity | 92 | 37 | - | 4 | - |

To avoid the lure of stories and the risk of succumbing to momentum traps, investors should be alert when strong momentum is paired with deteriorating fundamentals or excessive valuation. Momentum is one of the strongest drivers of returns in the stock market, and certainly capable of carrying story stocks some distance. But momentum can crash, particularly in shares with heady valuations and suspect quality.

It’s a message best summed up by Montier, who says the key is to focus on facts. “Focusing on the cold hard facts (soundly based in real numbers) is likely to be the best defence against the siren song of stories.”

The basic Momentum Traps screen can be found here. Subscribers can ‘Duplicate’ it to add it to ‘Your Screens’ and then tighten or loosen the rules according to preference.

To find out more about the taxonomy of stock market winners, you can browse through the entire series:

- Towards a taxonomy of stock market winners

- Contrarian stocks - how going against the crowd can put you ahead

- High Flyers - how to beat the market in expensive and highly priced shares

- Turnarounds - how to find value shares that are bouncing back

- Falling Stars - how to handle glamour shares that fall from grace

- Value Traps - how to avoid bargain stocks that might never recover

- Momentum Traps - how to avoid the siren song of overhyped stocks

- Sucker Stocks - why do we love to own the worst prospects in the market?

About Ben Hobson

Stockopedia writer, editor, researcher and interviewer!

Disclaimer - This is not financial advice. Our content is intended to be used and must be used for information and education purposes only. Please read our disclaimer and terms and conditions to understand our obligations.

Are we not having a lot of things here where QV is not a very good metric?

- Admiral is an unusual insurer so double problem for a balance-sheet based valuation

- the "new banks" (Aldermore, OneSavings) have a similar problem as banks and as new businesses

- Dignity is more like the junior tranche of a CDO than normal equity

- Severn Trent is a utility which also work funny

- Pre-release R&D bets like OPTI can't be valued on accounting data

Hi Ed, I totally get why OPTI might make this list, but as its a stock I own just wanted to make a case for the defence!

As its a company that doesn’t have any revenue streams (yet) but its stock price has multipled from 8p to a high of 56p recently, I can fully understand why this would be seen as blue sky and speculative; I don’t disagree on that. The investment case for OPTI for me is more based on a very impressive management team, low cash burn and very strong growth prospects going forward.

Basically, the CEO Dr Stephen O’Hara identified a couple of years ago that there was a specific gap in the market regarding the human micro biome and how to reprogram the role of bacteria with the human gut. Sounds pretty unappetising I know, but whereas as the likes of 4D Pharma are several years away from bringing anything to the market in the micro biome space, Optibiotix are reportedly on the verge of commercialisation for Cholesterol lowering food supplements. According to Tom Winnifrith, they are in advanced talks with Proctor and Gamble to bring this to market imminently. The results of human trials have not been revealed yet but hopes are high that Optibiotix will be able to deliver better results than market leader Benecol.

On top of this, they also have patented 7 more microbial strains, including novel sugars and weight loss capabilities. The potential here is pretty big and although speculative as an investment, I personally am a happy holder and have a lot of trust in Dr O’Hara’s approach. He and his team have so far hit every target they have set themselves and hopefully we will soon see the fruits of their labours. Bear in mind that 4D have a market cap of £463m and Optibiotix’s is £41m but are much closer to potential commercialisation and it’s not difficult to see why the stock has gathered so much momentum in the last 14 months.

As an aside, the biggest shame is that the bulletin boards have gone a bit bonkers about it, with a fair few nutters on there too. However, looking purely at the company and the fact that no-one else is currently in this space in the market I’m happy to hold. If it all goes down the pan fair enough, but as I’ve got my fair share of high stock rank stocks in my portfolio I feel I can make room for Optibiotix too.

@cig

Pre-release R&D bets like OPTI can't be valued on accounting data

That's so not true. Pre-revenue stocks are defined as 'junk' on the academic quality spectrum as they tend to be loss making. In aggregate portfolios of junk stocks have proven to be statistically losing bets. That's the whole point... story stocks always have a great sales pitch... but they tend to lead to dilution and disappointment - in aggregate on average. OPTI may be a wonder stock - but on average stocks like OPTI will disappoint.

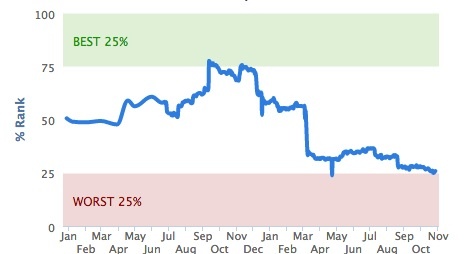

Regarding the others... I don't really buy your argument. These stocks all used to have much higher QV Scores - before their runs. For example here's Severn Trent's QV Score over the last couple of years. The stock has done really well and the QV score has dropped.

Admiral - QV Score - same again

I know when I'd have rather bought all the above !

Admittedly though the Quality Rank is not perfect for banks. I created a proprietary version for the TSB float which worked very well and pocketed me a 30% gain. We'd like to do separate Quality Ranks for REITs, Trusts and Banks... but that's a job for 2016.

Ed - did you generate those QV change charts behind the scenes or can us mere mortals create them too ? If so, how ?

Thanks, Ed. Interesting QV had predictive value here, though I still think from first principles normal valuation is inappropriate for these stocks in the long term because essential drivers of the business performance are effectively off-balance sheet (underwriting standards for insurers, regulatory relationships for utilities, etc). Maybe there's an opportunity here: if special stocks get priced classically in the short term but to their fundamentals long term, there will be juicy mispricings regularly.

I know story stocks are a bad deal as a class, I only meant to claim balance sheet valuation is not helpful to value them (rank them within their class if you wish). For eliminating the category, OK, low QV will work, though slightly overcomplicated, as any trivial "makes some money" test will catch them as well (I use "net income < 1m" in my own screens).

If you do bank-specific scoring, you should consider doing insurance as well, similar problem (if perhaps hard to do with a single model).

M.T. yes im beginning to see this with some of the junior gold stocks...be careful!!

Any ideas on how long Momentum Trap classification can last or is there a way of knowing when the car crash is about to arrive?

One of my best performing shares is ITM Power (LON:ITM) - it's been either a Sucker Stock or a Momentum Trap ever since I purchased it (long ago). I guess it is an ultimate "story stock" but have we got to wait until the company does start generating meaningful revenue and, I hope, profit before the Momentum Trap classification falls away?

I guess the same could be said of another of my holdings, IQE (LON:IQE) - I'm a glutton for stories and some of them do come true.

All the fuel cell shares have shot up in November after having had profit taking over recent months having been multibaggers in the year before Covid.The bellweather fuel cell stock is Ballard Power Systems and my guess is if that goes into downtrend all the other fuel cell shares will go into freefall .

Personally i have top sliced Fuel Cell profits and put them into platinum stocks as hydrogen fuel will need platinum but it is not 2 way . The platinum price could go up for other reasons than from Fuel Cell demand i.e platinum is a 'picks an d shovel' way of playing fuel cell but could avoid a fuel cell sub-sector freefall.

We have had ITM for a while now, bought as the result of a factory visit, to see the good work that was being done, and understanding their orderbook and moreover the effect of CV-19 on their business. Momentum trap or not we will stay with them.

Caution is aired with those that have a strong averse to risk management. Setups like a volatility contraction pattern with strong confluence at support on HTF's have a very high chance of success. Don't take my word for it. do the back testing on any phase 2 uptrend stock and make sure the VCP has contractions less than 10% as it breaks a base. then have an exit strategy and move up your stops as it rains profits. This is not financial advice

Mmmm - interesting thoughts. However, if you are looking as a long term investor rather than a trader, then momentum is meaningless - today's overpriced is tomorrows bargain. I prefer to look more at the long term fundamentals of the stock:

1. Is it in a disruptive and growing market

2. Does it have a good track record of growth and hitting/beating expectations

3. Is the management team of good quality and are they committed to the company and the market

4. Do I believe in the quality and differentiation of the product or service they offer.

As they say form (momentum) is temporary; class (fundamentals) is permanent

*Past performance is no indicator of future performance. Performance returns are based on hypothetical scenarios and do not represent an actual investment.

This site cannot substitute for professional investment advice or independent factual verification. To use Stockopedia, you must accept our Terms of Use, Privacy and Disclaimer & FSG. All services are provided by Stockopedia Ltd, United Kingdom (company number 06367267). For Australian users: Stockopedia Ltd, ABN 39 757 874 670 is a Corporate Authorised Representative of Daylight Financial Group Pty Ltd ABN 77 633 984 773, AFSL 521404.

A1MHigh just tweeted that OptiBiotix Health (LON:OPTI) should be on this list

It's not making the screener cut as it's too small (MktCap £40m odd) but yep I'd have to agree from the numbers this looks a hype stock.

Please add your own Momentum Traps to the comments here.