It’s not too late to invest in the resources boom: ideas for 2023

In this article:

Why the mining sector is more appealing to generalist investors than it has been in the past (hint: it’s associated with the tech sector and the green energy revolution)

How the long-term demand for certain resources is obscured by short-term supply trends

What you need to know about how the cyclicality of mining and the timing of capital expenditure projects affects returns

Which miners are worth taking a closer look at in 2023

I have never given the resources sector the attention it perhaps deserves. I like to invest in (and write about) companies which make exceptional profits off products and services which the world relies on. Mining, which is capital intensive and at the very bottom of the supply chain, is about as far removed from my sphere of interest as it gets.

But I also love to research companies that are genuinely investing in making the world a better place - renewable energy or next generation healthcare, for example. In 2023, with high-growth stocks in free fall, the resources sector has become a far more attractive way to gain exposure to hot trends like electric cars and the green energy revolution.

And so I have endeavoured to become better acquainted with the sector in order to give myself a fighting chance of unearthing (no pun intended) opportunities. My thanks to Keelan Cooper, for patiently sharing his experience of investing in the sector.

Demand dynamics: The need for raw materials

In this section:

Technological progress is expected to have a big impact on the energy, healthcare and industrial markets in the coming decades

Minerals extracted from the earth will be crucial to powering the tech of the future

Some of the world’s pessimists say that the human race has not put its technological prowess to good use in the last few decades. In his book The Rise and Fall of American Growth, Robert Gordon imagines the surprise a person who fell asleep in the 1870s and awoke at the dawn of the second world war would have in seeing the telephone, the lightbulb, cars and x-rays. Whereas one who took a nap in 1940 would not be introduced to anything completely new when they woke up in the early 2000s.

I consider myself one of those pessimists. In the last few decades we have decoded the human genome but health outcomes have barely improved. We have created microchips which carry the same computing power Neil Armstrong took to the moon, but use them to share pictures of our food on social media. We have split water molecules to create energy, but still heat our homes with high carbon fuel drilled out of the ground.

This phenomenon was captured succinctly by the American scientist Roy Amara who said “we tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run”. I believe that we are currently in a period of underestimation: the technological breakthroughs of the late 20th century have not yet achieved their full potential.

But they’re getting there. The coming decades are likely to see a big change in the way we use technology. We’ll travel in electric vehicles, some of which might be autonomous. Consumer goods will be made in factories which are automated, just like the logistics and distribution centres. Robots will also be used to supplement human-delivered education and healthcare. And all these robots will rely on enormous data systems which, just like our homes, offices, factories and hospitals, are powered with a mixture of gas, renewables and nuclear.

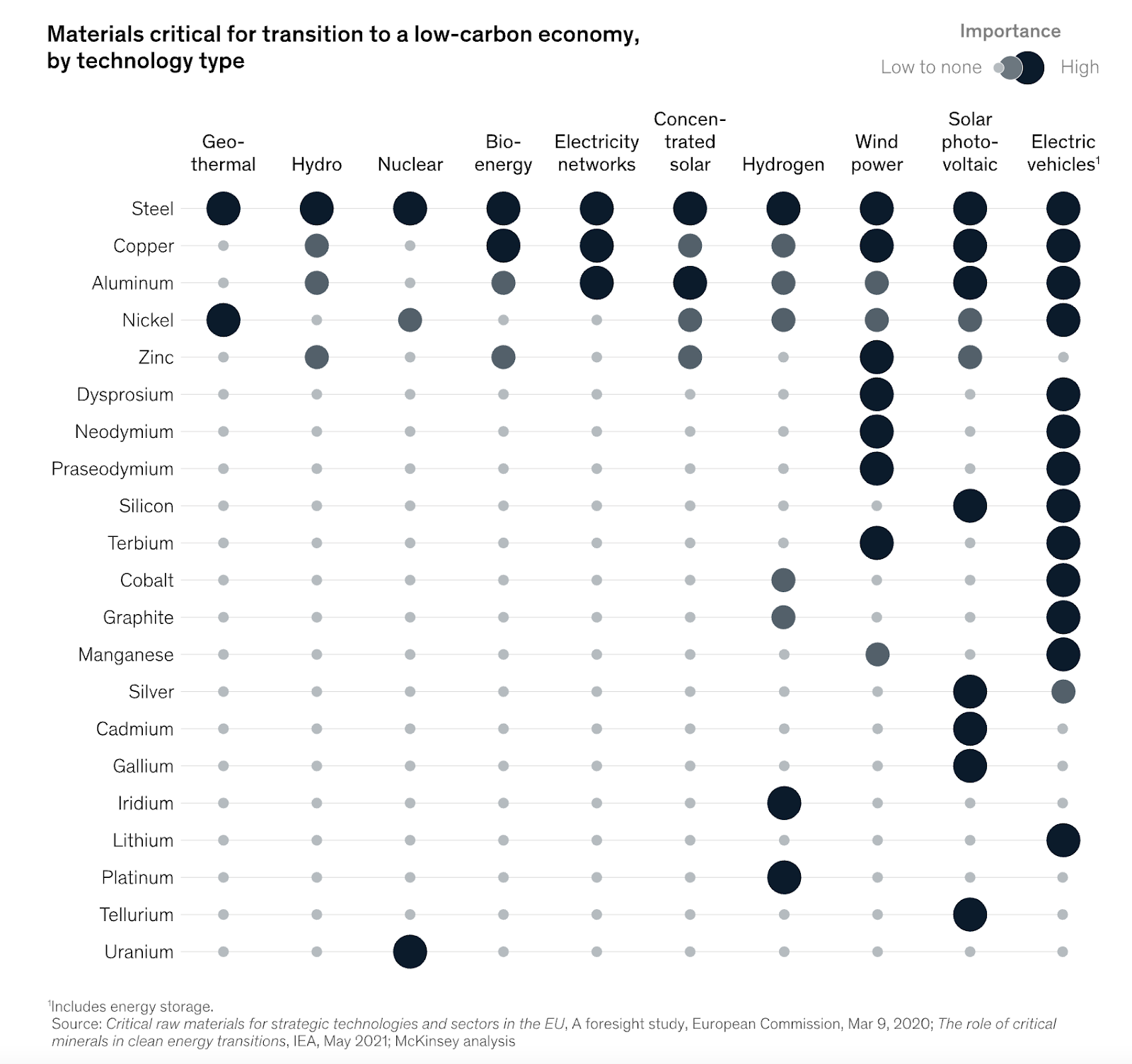

And so, by a somewhat circuitous route (I did say I liked writing about the tech sector) we arrive back at the point of this article: resources. To build our electric vehicles, data centres and nuclear energy plants, we need to mine the materials for them out of the ground. Cobalt, lithium and nickel, for example, are crucial elements in electric vehicle batteries. Copper and zinc are needed in solar and wind farms. Aluminium, steel and platinum are used in semiconductor and other tech elements. You can see more of the crucial resources required for powering the future in the chart below.

2023: Supply-side constraint and short-term disruption

In this section:

In 2022, commodities prices boomed as strong long-term demand met tight supply

Prices have remained high going into 2023 as the miners hesitate to invest in new capex projects (and rejig the supply and demand imbalance)

Investing in the mining sector requires knowledge of the nuance of capex projects - when miners start investing, the prices of the commodities they are mining tends to fall

Given the surge in demand expected in the coming decades, you might expect miners to be investing heavily in adding capacity. But short-term distractions mean that, for now, big investment projects aren’t being switched on.

For example, in 2022, supply chain disruption in the manufacturing industry tempered immediate demand for battery metals including lithium, nickel and cobalt, thus masking the major long-term deficits. Copper and steel demand has been hampered by a weakening global property market (although the recent removal of China’s zero-Covid policy is expected to reverse this trend slightly). And then there is inflation in energy costs and rising interest rates, which sent up the cost of financing projects and dampened the outlook for exploration in 2022 and early 2023. The result was a widening of the deficit in some of the key materials of the future.

This tight supply supported record prices across the commodity market. True, prices aren’t climbing in a linear fashion (that’s not how the resources market works), but new highs have tended to be higher than their previous highs - evidence of a commodities super-cycle in play.

And yet, many companies (especially those which mine ‘old-world’ resources) are still hesitant to embark on big capex projects. Why? Because management chooses to invest if they are appropriately rewarded. This phenomenon has baffled me as a newcomer to the sector - if individual commodity prices are currently high, surely everyone will benefit if the miners start drilling again?

The reality is more nuanced. Despite high commodities prices (and the relative strength of the sector compared to other industries), miners are not likely to be fully rewarded by their investors for turning on the capex taps right now because those investors are still nervous. And rightly so as their most recent experience of capex investment was a bad one - according to Goldman Sachs, US exploration and production companies destroyed $0.54 for every dollar they invested over the last cycle (2011-2020).

These conditions suggest that we are currently in ‘Stage 1’ of the cycle, characterised by:

High commodity prices

Inflation pushing interest rates up

High capital costs tempering investor appetite for prolonged capex projects

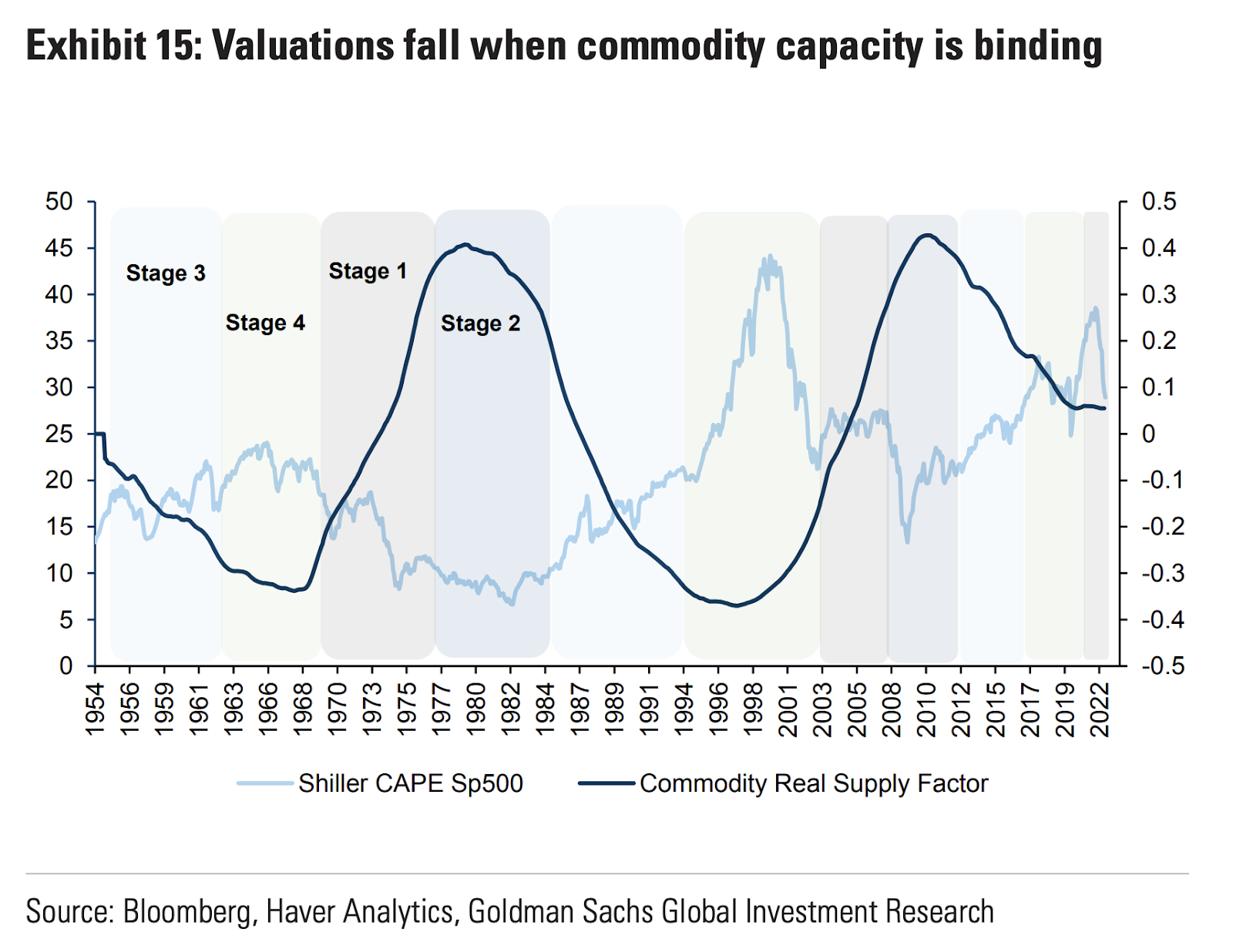

The sector will only move into Stage 2 when miners begin to be appropriately rewarded for capex investment. At which point commodity prices are expected to fall. The chart below shows how commodity prices have moved through investment cycles in the past.

This chart also provides evidence for an imminent resumption of capital spending as the three-year Sharpe Ratio of the commodities sector is beginning to fall. The Sharpe ratio is a measure of risk adjusted returns when the commodities ratio has started to converge with the Sharpe Ratio of the Nasdaq in the past, capex projects have been resumed. Put plainly, when the risk-adjusted returns of the mining sector start to look superior to that of the tech-heavy Nasdaq, conditions are ripe for capex projects to begin.

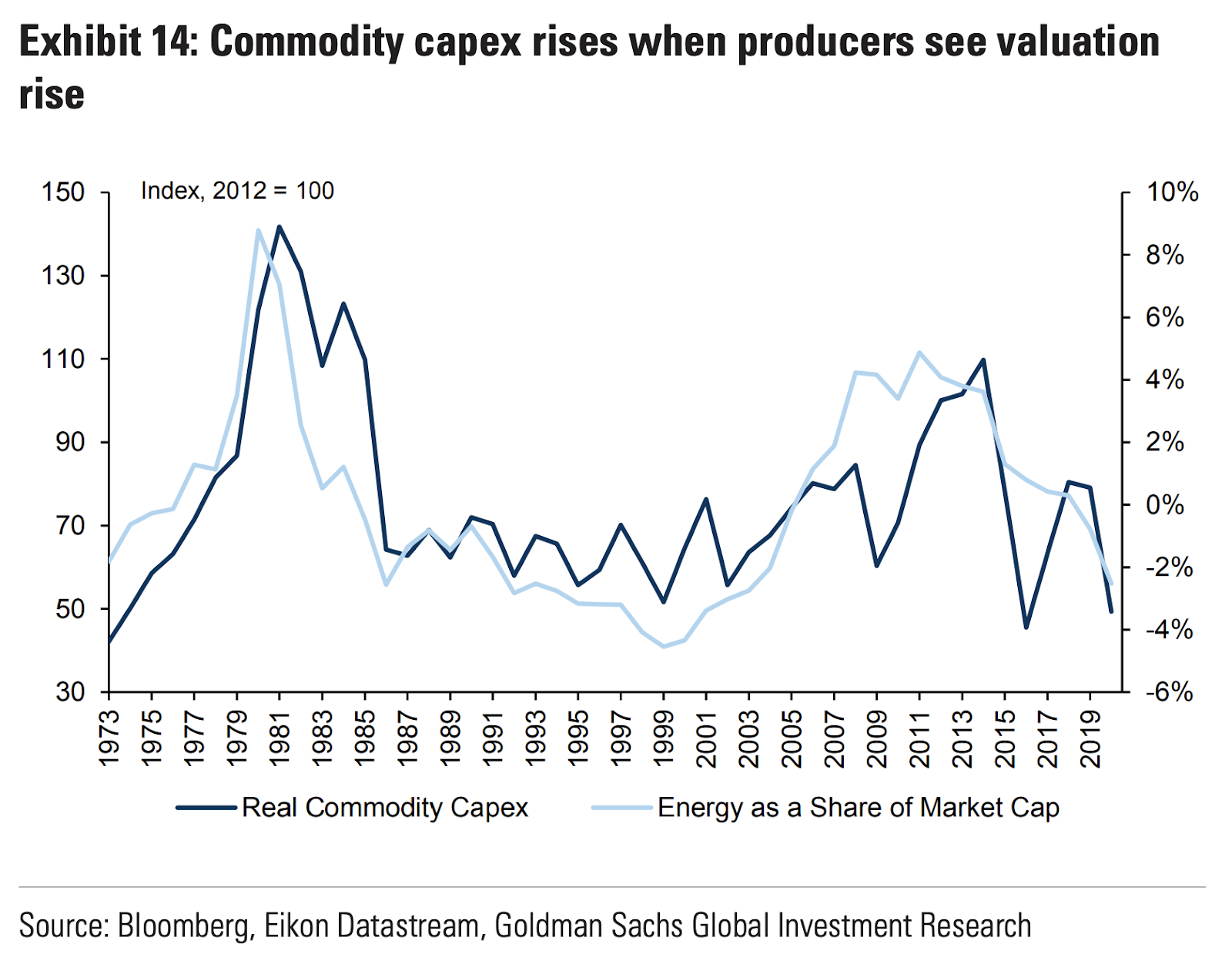

More broadly, the relaxation of Covid-rules in China and a softening of the Federal Reserve base rates could see more projects starting to come back online as 2023 progresses. As demonstrated by the chart, commodity capex tends to rise when producers see their valuations rise.

Economics of pricing: weather all storms

In this section:

The short-term outlook for the miners is mixed - if they start investing prices are expected to fall

The companies with the lowest all-in-sustaining-costs (AISC) will still be able to profit if prices fall

The traditional capex cycle is being disrupted by long-term trends

And so, in 2023 industry experts are expecting miners to switch on their pipelines again, thus closing the short-term supply and demand imbalance and putting pressure on prices. It is worth noting that current pipelines are not nearly enough to close the long-term supply gap, but in many cases the short-term demand is likely to be met simply by an immediate increase in drilling. For example, lithium, cobalt and nickel are forecast to be in surplus in 2023 and 2024 - after all, EV battery demand is being ramped up, but isn’t likely to hit the ambitious targets for the next few years.

So, investors who go hunting in the sector should be on the lookout for companies with the operational efficiencies to weather all storms. The table below compares the current spot prices and the outlook for selected metals with the all-in-sustaining costs for some of the biggest miners.

The companies which can make profits on even the lowest forecast spot prices are best placed to thrive in the coming capex cycle.

But in this cycle there are other dynamics at play, namely the influence of green initiatives and technology.

For example, miners with high ESG scores have far easier access to capital than those for whom social and environmental matters are ignored. A recent report from McKinsey found that the cost of capital for miners with low ESG scores is between 20% and 25% higher than their greener peers. Many manufacturers also have green targets to hit and therefore seek to source their raw materials from miners which are attempting to decarbonise. The road to ‘zero-carbon’ mines might seem a long way off, but improvements in operational efficiencies and greater use of carbon-free fuels in haulage and drilling are helping many of these companies make significant reductions to their carbon emissions. The likes of BHP and Brazilian miner Vale are targeting a 30% reduction in carbon emissions by the end of the decade.

These companies are simultaneously making sizeable investments in their technology. New systems can improve the operational efficiencies of mines helping extract more minerals for equal effort. This is especially important for the resources that are in high demand, such as lithium, where demand is forecast to increase eightfold by the end of the decade. Direct lithium extraction from unconventional sources (such as geothermal fields or oil wastewater) is a process which is being explored by some of the forward-thinking miners in the sector.

An eye on the future

In this section:

Long-term demand is forecast to create massive supply deficits for battery metals

Iron-ore, zinc and copper are more likely to see a short-term deficit, but longer-term surplus

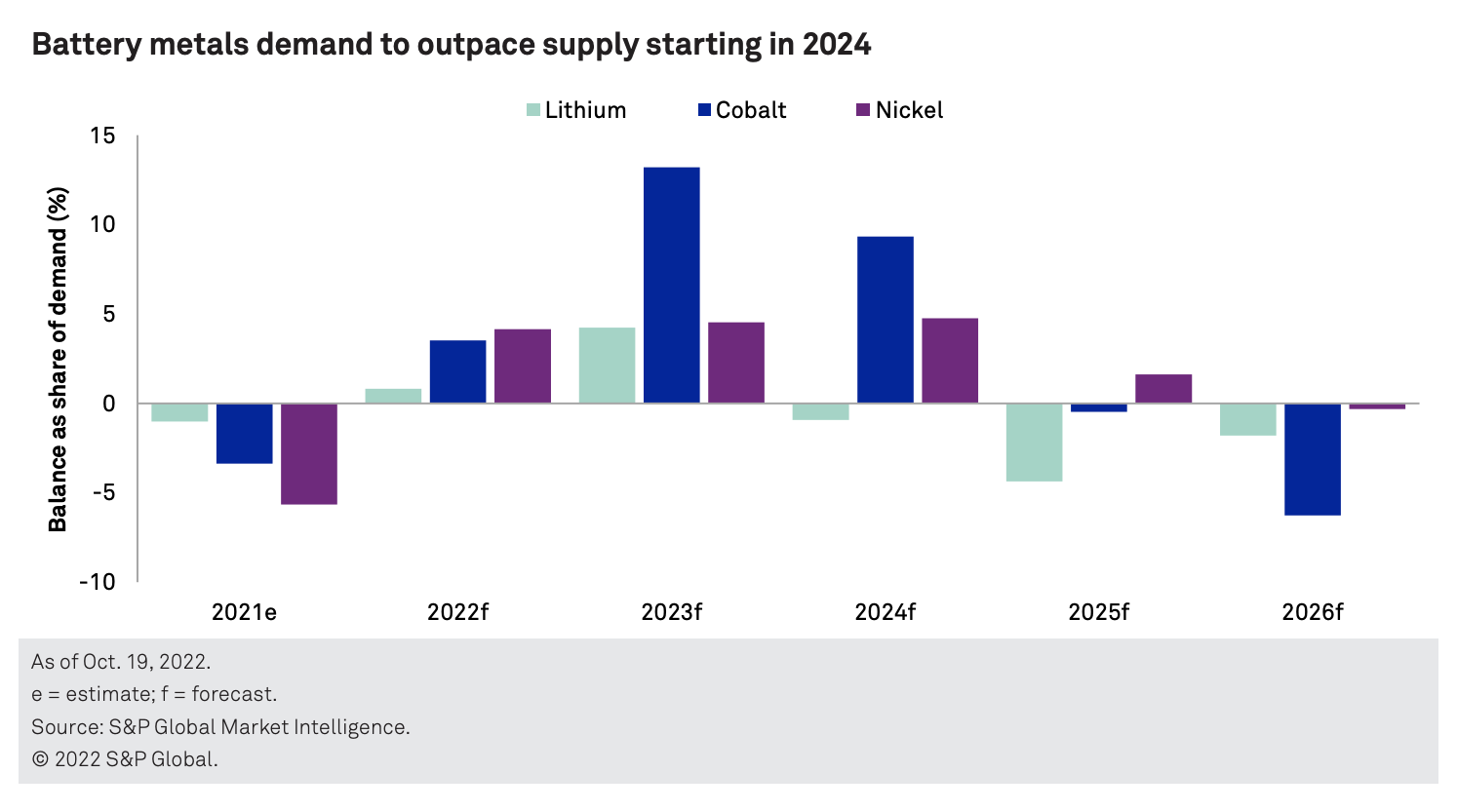

But while these short-term supply dynamics are important for investors to understand, it’s the long-term outlook where the big opportunities lie. Current pipelines and capex projects won’t be able to fill the demand for certain resources meaning prices are likely to rise again and the companies with exposure to these resources will be rewarded. For example, it is forecasted that by 2030 EV makers will require almost 10m tonnes of lithium a year, up from 0.5m tonnes last year.

The chart below shows the demand/supply imbalances that are forecast for the key resources required for EV batteries, where sales growth is expected at a compound rate of 28% a year:

Lithium is expected to be in a deficit as early as 2024

There is a healthy supply of cobalt (largely from mines in the Democratic Republic of the Congo) until 2024, but by the following year it will have also fallen into deficit

Indonesian supply of nickel is expected to keep up with demand until 2026 when EV when battery-related demand for nickel is forecast to hit 17.6% of all nickel demand — up from 7.1% in 2021

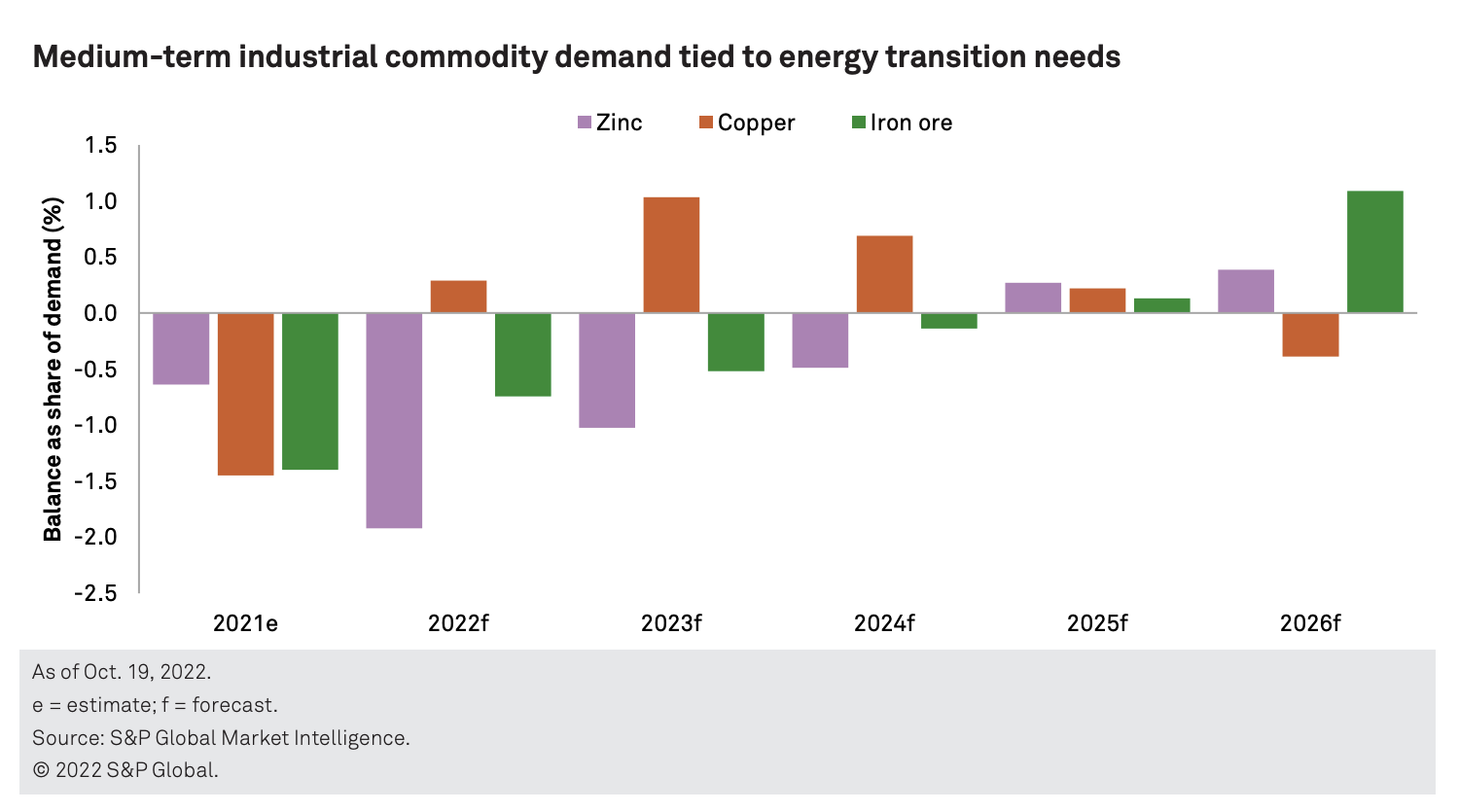

The outlook for more traditional resources including copper, zinc and iron ore is also being impacted by the energy transition. All three will be required for wind farms and solar cells, but as the upswing in demand is not forecast to be quite as stark as the battery sector, these resources are less likely to see a long-term deficit - as demonstrated by the chart below.

Identifying mining ideas

In this section:

A screen to identify a long list of reliable mining stocks

Analysis of how much exposure various miners have to ‘new world’ resources

I’ve drawn up a long-list of potential opportunities using a very simple screen which identifies miners with a strong track record of high operating margins (to ensure that they can withstand a drop in commodities prices), currently trading on a reasonable price to earnings ratio (to ensure that they are profitable and their exposure to long-term trends isn’t already priced in). I have also limited my search only to miners located in the UK, US, Canada and Australia (which are well established).

You can see the full results of that screen here, but beware you won’t be able to see the full screen results without international markets in your subscription.

From that screen I have identified a handful of miners which have exposure (or at least have started investing) in the resources required to power the future. These are shown in the table below.

Country | Name | Op Mgn 5y Avg (%) | P / E Forecast 1y | Mining Exposure |

au | BHP (ASX:BHP) | 41.17 | 11.28 | Copper Nickel Potash |

gb | Rio Tinto (LON:RIO) | 37.69 | 9.04 | Aluminium Copper Lithium |

gb | Anglo American (LON:AAL) | 25.63 | 9.41 | Copper Nickel Platinum |

au | Mineral Resources (ASX:MIN) | 35.42 | 10.06 | Lithium |

ca | Lundin Mining (TSE:LUN) | 25.61 | 15.00 | Copper Zinc Nickel |

au | Nickel Industries (ASX:NIC) | 22.75 | 13.99 | Nickel |

gb | Central Asia Metals (LON:CAML) | 45.86 | 7.29 | Zinc Copper |

gb | Kenmare Resources (LON:KMR) | 21.44 | 2.98 | Zircon |

gb | Ecora Resources (LON:ECOR) | 68.90 | 4.37 | Copper Cobalt Nickel Vanadium |

gb | Jubilee Metals (LON:JLP) | 20.91 | 12.30 | Copper Phosphate Zinc Nickel |

gb | Sylvania Platinum (LON:SLP) | 45.36 | 4.97 | Platinum |

gb | Griffin Mining (LON:GFM) | 30.31 | 9.98 | Zinc |

Source: Stockopedia, company presentations | ||||

And from there I have gone on to analyse the difference between the all in sustaining costs and spot prices of resources currently being mined, leaving me with a far more focused list of potential opportunities. There is still more research to be done (keep a look out for more detailed research into certain stock picks in the coming weeks).

Name | AISC |

BHP | Iron Ore: $16.81/t Copper: $1.20/lb Coal: $70.8/t |

Rio Tinto | Iron Ore: $22.5/t Copper: $1.80/lb |

Anglo American | Iron Ore: $40/t Copper: $1.59lb Nickel: $4.95/lb |

Lundin Mining | Copper: $1.92/lb Zinc: $0.18/lb Nickel: $1.05/lb |

Nickel Industries | Nickel: $4.61/lb |

Central Asia Metals | Copper: $0.57/lb Zinc: $0.63/lb Lead: $0.63/lb |

Kenmare Resources | Zircon: $105/t |

Jubilee Metals | Copper: $1.81/lb Phosphate: $4.56/lb |

Sylvania Platinum | Platinum: $6.46/oz |

Source: Stockopedia, company presentations | |

There is, of course, a lot I haven’t covered in this overview of the miners. Uranium mining, for example, has huge potential for changing dynamics as the nuclear energy debate gathers momentum (perhaps a topic we’ll explore more in the future). And there is gold or precious metal mining, which is highly topical in the current inflationary environment - but again, that’s a topic for another day.

About Megan Boxall

Disclaimer - This is not financial advice. Our content is intended to be used and must be used for information and education purposes only. Please read our disclaimer and terms and conditions to understand our obligations.

Andrada Mining (LON:ATM) : Soon to be the only producing lithium company on AIM. And they are producing the lithium at an AISC of $0. The lithium has been dumped in tailings up until this year when they have built the lithium plant. Main product is tin which they now produce 720t per year, that's what pays the bills at the current £30k/t, but the lithium is the game changer.

I wondered why I hadn’t heard of them…. I see it’s Afritin with a new name. I think with small cap miners it’s important to make distinctions between producers & explorers, money is made by being in at the right relative stage. Just now imo, producers are the place to be, the more speculative explorers will spike at some point but I don’t anticipate that any time soon. Just my thoughts.

2, Major change you overlooked in 1949 was the invention of the transistor which led to integrated circuits and very large scale integration and modern computers, TVs etc.

Many thanks Megan. As others have commented, it's great to see an article on resource stocks on Stocko as that is a major gap In its overall analysis in my view and represents an area that my investments are currently weighted towards. . There are lots of paid marketing companies in the sector and it's difficult to get independent analysis and see the wood from the trees. I'm looking forward to the next article on this sector.

Thanks Megan, your articles have much improved since your very first ones where perhaps you were quoting too much metric data from Stockopedia, something we are able to find ourselves. In fact, I like your articles even more than the others now. Would you consider doing some similar research into oil and gas stocks as you have done here for mining?

Good article Megan. The thought I would add is to look at the picks and shovels plays on resource mining, companies like Weir but also, of higher quality and larger scale, Caterpillar, Sandvik and Epiroc, all of which have rebounded hard from the October lows, like much else. As a buy and forget investment for the next 20 years, I would have thought these were a less volatile and lower risk choice to play the theme. But seekers of value will have to wait for a dip, which may come shortly.

Great article. It amazes me that anyone takes the LME seriously but that’s another matter after they let slide the blatant manipulation of Nickel. Suggest there are three producers of Lithium Hydroxide, this is the product. Australian stocks PLS, MIN, IGO, AKE. These companies currently produce more than 30% of world demand. Cheers.

Thanks for another great article. Its good to see resources discussed in detail. I'd suggest a look on YouTube at the portfoliomatters posts which have a similar focus but include oil

I think you have missed mentioning Phoenix Copper (LON:PXC) (I hold) - not yet in production, but this share has started to rise rapidly over the last couple of weeks in anticipation of financing news (by end of Feb, we hope). They have a lot of critical minerals in a very safe mining jurisdiction (Idaho), an excellent and experienced management team, deep respect for their shareholders and a promise not to dilute shares by utilising their low hanging Empire Open Pit Mine to finance exploration across their other sites... watch this space for a winner IMO ;-) .

You could consider ASX listed MRC which owns the Skaland graphite mine in Norway. This mine is the fourth largest crystalline graphite producer in the world outside of China and accounts for around 2% of global flake annual graphite production. It also owns a graphite deposit in Western Australia which it is looking to develop.

It is not a pure graphite play also owning mineral sand operations in South Africa. Definitely worth doing your research on this one before investing though as they have had some issues recently. If it can sort itself out and graphite takes off now could be a good time to acquire shares in MRC relatively cheaply.

Does anyone know why tin is down so much today? Wisdomtree Commodity Securities (LON:TINM) is down over 6%.

*Past performance is no indicator of future performance. Performance returns are based on hypothetical scenarios and do not represent an actual investment.

This site cannot substitute for professional investment advice or independent factual verification. To use Stockopedia, you must accept our Terms of Use, Privacy and Disclaimer & FSG. All services are provided by Stockopedia Ltd, United Kingdom (company number 06367267). For Australian users: Stockopedia Ltd, ABN 39 757 874 670 is a Corporate Authorised Representative of Daylight Financial Group Pty Ltd ABN 77 633 984 773, AFSL 521404.

Sylvania Platinum with an AISC of $6.46/oz ? Yes please!