Covid Stocks: A good investment in today’s markets

We have written a lot in recent weeks about the use of factors during various stages of a market cycle. To summarise: momentum has defensive qualities which keep stocks propped up when markets are crashing, value has the highest propensity to recover in the immediate aftermath of a sell-off and the StockRanks have a track record of wealth protection during financial crises. We’ve also examined sector trends and speculated that it might be too early to switch to cyclicals to take advantage of big price drops.

So where to invest right now?

Fighting my natural (bear market first-timer) instinct to pick stocks that I like which have sold off extensively and now look better value than they have done for the last couple of years, I have used Stockopedia’s screening tools to find stocks which are not tied to the market cycle (defensives), display high quality, decent value metrics (high QV StockRank), but have underperformed their own market (relative share price trend less than 0% in the last year).

Limiting my selection to companies larger than £1bn and broadening my remit outside of the UK (where my screen’s output left me uninspired) resulted in a selection of 34 US stocks, two of which caught my eye: Moderna (US: MRNA) and BioNTech (US: BNTX).

A blast from the Covid-past

When Covid-19 first arrived in the US in early 2020, BioNTech had only been listed on the public markets for a few months. The company had endured a relatively humiliating IPO which saw it valued at $3.4bn - below the valuation given at its most recent private fundraising. Still BioNTech joined Moderna as one of the biggest biopharma IPOs of the decade, with both companies seeking to contribute to America’s burgeoning immunotherapy market, where patients’ own immune systems are coerced into fighting diseases such as cancer.

And then came Covid-19 and the world looked to pharmaceutical companies with immune system expertise. At the time BioNTech had a number of potential immunotherapies for ten different infectious diseases but no plans to take them into clinical trials until 2021. Moderna had six vaccine candidates in clinical trials for rare infectious diseases and an innovative platform for identifying new immunotherapies at pace. By March 2020 both companies had selected novel vaccine candidates for the protection against what was then known as ‘a novel coronavirus’ and had received additional funding to fast-track clinical trials. In the first quarter of 2020 - the worst for global markets since the 2008 financial crisis - both companies' share prices had risen more than 50%.

With more funding secured under the US government’s ‘Operation Warp Speed’ programme, Moderna and BioNTech successfully completed small scale human safety trials in August and in November BioNTech’s candidate had been approved for use in the UK - the first Covid-19 vaccine available in Western markets. By December both companies’ vaccines had been granted Emergency Use Authorisation by the US Food and Drug Authority (FDA) - a notoriously hard regulatory body to satisfy.

The speed at which BioNtech and Moderna morphed from early stage R&D companies to commercial operations with the world’s most sought after vaccine had a marked effect on their business profile.

In the 2020 financial year, both companies’ research and development expenditure more than tripled. But by 2021 they had started generating serious revenues from the vaccines. Sales at BioNTech rose from €109m in 2019 - mostly generated from R&D credits from big pharma partners - to €18.9bn in 2021. At Moderna the pattern is similar: $60.2bn of sales in 2019 versus $18.5bn in 2021. This leap helped both companies generate their first operating profits in 2021 and forecasts suggest they will continue generating significant revenues from their Covid-19 vaccines in 2022. BioNTech estimates between €13bn and €17bn of sales, Moderna had recorded advanced purchase agreements worth $21bn by August of this year.

The future in immunotherapy

But a pandemic which requires a global vaccine roll-out is (hopefully) a once in a lifetime experience and while Moderna and BioNTech will no doubt continue to generate some sales from ongoing booster jabs, demand for Covid-19 vaccines will be nothing like that seen in 2021. Indeed, Moderna is clearly concerned about ongoing competition for sales because it has filed a lawsuit against BioNTech (and its big pharma partner Pfizer) in the US and Germany for patent infringement. Moderna claims that BioNTech’s vaccine copied the technology which it had developed and registered in the decade leading up to the pandemic. The company isn’t seeking removal of the product from the market, but is looking to acquire monetary damages for patent infringement.

Investors know that the best days in virus vaccination are over and have responded as expected. BioNTech’s share price has fallen 66% from its peak in mid-2021 when it reached a market capitalisation of over $100bn. Moderna stock is currently worth about $40bn, from a high of $140bn in August 2021.

And their future is firmly in immunotherapy. BioNTech has five cancer treatments in the second phase of clinical trials and a further 16 in the first phase. Many of these already have a big pharma partner which will help with the manufacture and roll-out. Alongside Pfizer - its partner for its Covid-19 vaccine - the group is also completing a phase three trial into a seasonal influenza vaccine which can help protect against specific strains of the virus identified by the World Health Organisation. Moderna’s suite of virus fighting vaccines is even more extensive. Alongside candidates for Covid-19 and influenza, the company is testing vaccines which protect against HIV and Zika. Its personalised cancer vaccine - which it is building alongside Merck (the global leader in immunotherapies) - is currently in the second phase of clinical trials.

It’s true that there are hundreds of biotech companies worldwide which are sitting on the same type of technology, many of which will be battling through clinical trials. But clinical trials are enormously expensive and many of the companies with promising technology simply won’t be able to afford to test their drugs in humans. It is here that Moderna and BioNTech stand apart from the rest. BioNTech has close to €10bn of net cash on its balance sheet, equivalent to nearly 10 years of R&D expenditure at current levels. Moderna has $17.6bn of cash which will allow it to keep spending on developing drugs at its current pace for almost nine years. What’s more, both of these companies are currently generating operating cash flows which is almost unheard of in early stage drug developers. True, these cash flows might come under pressure as Covid-19 vaccine sales slow, but for now the companies are in a far stronger financial position than many of their peers.

What’s more, they have experience commercialising a drug and fast tracking it through the FDA if demand is high enough. With big pharma partners and global recognition, the path to regulatory approval could be smoother for the heroes of Covid-19 than other biotech companies. Perhaps a small-silver lining from the pandemic pain of the last few years.

About Megan Boxall

Disclaimer - This is not financial advice. Our content is intended to be used and must be used for information and education purposes only. Please read our disclaimer and terms and conditions to understand our obligations.

It's great to have international stocks featured, which happens WAY too infrequently. Around 80% of my holdings are international, and this site's focus on UK stocks - particularly small caps - needs to change IMHO. So well done, Megan...!! Plus an interesting thesis - I will definitely look into it.

I agree with the earlier comment. So refreshing not just having small caps. I left stockopedia a couple of years ago for this very reason but thought I’d give them another go - but no change!

Come on guys widen the chat

Lorna, There are more posts now on large caps and international stocks but few responses from members. Problem is there are so many stocks to cover.

I did try the US region but it did not work for me, pity as I'm looking to invest more there. UK small caps can be good in the right market.

Whilst I agree in principle with your main point, it’s good to see the additional range of stocks commented on. But this site is mainly about providing tools to help individuals research and screen.

Rather than bleat about it…. Why don’t you post something yourself and generate a discussion in areas of interest to you?

At the moment my entire portfolio is made up of the FTSE All Share. However, recently I have extended my subscription to include US stocks too. This has allowed me to tighten my screening criteria considerably, so much so that Shell is now the only UK stock that qualifies. I am not going to suddenly sell all my UK stocks, but I shall now use threshold rebalancing of my portfolio and gradually replace stocks when they drop below a stockrank of <73 and add in a new, stricter criteria, mainly US stock, By the way, most tend to be large and mid-cap stocks, no small stocks have qualified at present.

I am surprised at this article. Though both shares have good stock ranks (92 and 88), a cursory look at forecasts shows that both companies are losing sales and profits. The case for them is therefore mainly a "story", something Stockopedia is normally keen to avoid. Incidentally, Hargreaves Lansdown will not allow me to purchase more Biontech in my ISA, for some technical reason, though I am allowed to hold onto what I already have.

I am surprised at this article. Though both shares have good stock ranks (92 and 88), a cursory look at forecasts shows that both companies are losing sales and profits. The case for them is therefore mainly a "story", something Stockopedia is normally keen to avoid

My thoughts entirely. There are hundreds of companies of the highest quality and track record in the US. Notwithstanding the depth of the article, these are companies whose financial futures are particularly unknowable. Let’s talk semiconductors or industrial automation or renewables or frankly anything other than biotech.

Both of these comments are 'non sequiturs'.

1) If the shares discussed have good stock ranks then they are not story stocks.

Some of Cathy Wood's Ark G genomics stocks have dubious value but it is not the case of the two put forward here.

2) Biotech is advancing while semi-conductors are declining.

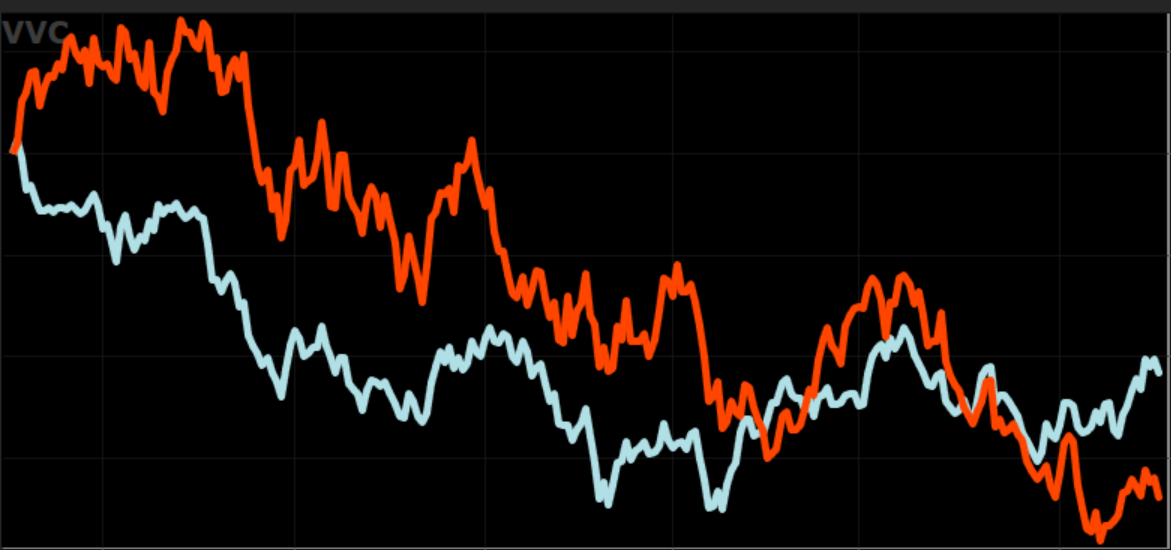

The 12 month chart below is IBB (etf for Biotech sector) v SMH in red (Semiconductors)

*Past performance is no indicator of future performance. Performance returns are based on hypothetical scenarios and do not represent an actual investment.

This site cannot substitute for professional investment advice or independent factual verification. To use Stockopedia, you must accept our Terms of Use, Privacy and Disclaimer & FSG. All services are provided by Stockopedia Ltd, United Kingdom (company number 06367267). For Australian users: Stockopedia Ltd, ABN 39 757 874 670 is a Corporate Authorised Representative of Daylight Financial Group Pty Ltd ABN 77 633 984 773, AFSL 521404.

Hmm..........

BNTX is 70% owned by two GmbH corps with the effect on up and down movements that comes with limited free float.

The chart shows it bouncing along the bottom for this year.

No trend.

Value, although my EPS graph shows a downward trend.

Worth investigation.

Thank-you.

Never heard of it before.

By the way in the text there was a phrase that may need attention:

At Moderna the pattern is similar: $60.2bn of sales in 2019 versus $18.5bn in 2021.