Building a Terry Smith portfolio with UK shares

Terry Smith’s annual letter to investors in his Fundsmith Equity Fund has become something of an event. He’s opinionated, informed, and usually has something spicy to say.

This year’s letter came with an extra dose of anticipation, as we knew Smith would have to discuss why the Fundsmith Equity Fund fell in value and underperformed global equity markets last year. A rare event indeed.

Megan reviewed Terry Smith’s letter in depth recently, so I won’t repeat her comments here. But one idea from the letter that caught my interest was the possibility that the kind of quality companies Fundsmith buys are now more attractively valued than they have been in recent years.

Sure, the fund fell last year. But for long-term investors wanting to buy shares in quality businesses, falling share prices are often good news.

I started to wonder. If I tried to build a portfolio of UK shares Terry Smith might buy today, what might I end up with? Would they be companies I’d want to buy today?

I decided to build a stock screen to try and find out.

Reading the manual

One thing that Terry Smith and Warren Buffett have in common is that they don’t mind sharing details of their investment approach. Fundsmith provides an owner’s manual on its website that provides a very clear description of the kind of companies the fund buys, and the financial metrics on which Smith and his team focus.

To refresh my memory, I reread the owner’s manual and noted down the key criteria Fundsmith uses to assess stocks. I then checked the website for the fund’s current sector weightings and top holdings.

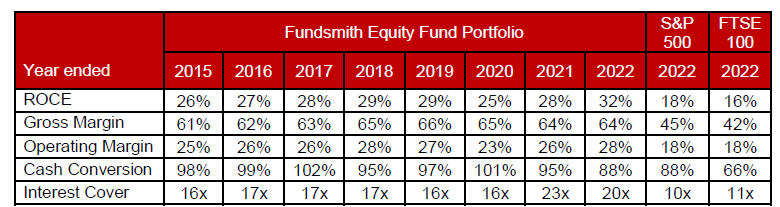

Finally, I looked at the table of portfolio financial metrics that’s always included in Fundsmith’s annual letter. This shows the weighted average financial characteristics of the fund’s portfolio, as if it were a single company. I’m a big fan of this technique, which Ed wrote about last year in “The perfect stock does not exist…”.

Source: Fundsmith 2022 annual letter

Armed with this information, I built a screen which I think highlights stocks Smith might consider, if he restricted his investment universe to the UK instead of investing globally.

Terry Smith screening criteria

Fundsmith’s stated investment strategy is:

Buy good companies

Don’t overpay

Do nothing

In this section, I’ll explain how I’ve tried to translate this deceptively simple three-step process into a set of screening rules, using Smith’s letter and owner’s manual as a guide.

I’ve linked to my Terry Smith screen here and have included a list of the stocks it produces at the end of this piece.

Sectors: The Fundsmith Equity Fund doesn’t have fixed sector allocations. Smith says he doesn’t pay much attention to sector weightings at any one time. However, the fund only invests in certain sectors of the market.

Broadly speaking, the fund aims to invest in companies that provide goods and services that are consumed in small quantities, at short and regular intervals. Consumer goods and online services are the obvious examples, but payment processors such as Visa (NYQ:V) are another example.

Heavily cyclical sectors are excluded, as are businesses selling capital goods that tend to generate lumpy revenues. Property and most financials are also ruled out, as these businesses tend to require leverage in order to generate satisfactory returns.

Smith doesn’t mind leverage, but he doesn’t like companies that can’t function without it. Banks and property are typical examples of this, but interestingly he also includes retailers’ large store lease liabilities in this category as well.

This approach is convenient for UK investors, because operating leases are included in statutory net debt under IFRS 16 rules. That means we can easily use this figure in our screening without needing to consider adjustments.

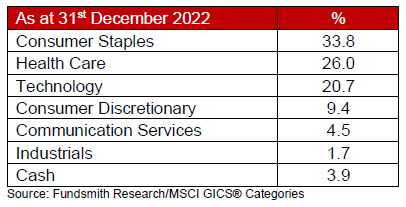

Here’s how the Fundsmith Equity Fund was positioned at the end of 2022:

Source: Fundsmith 2022 annual letter

I’ve translated this to the following UK market sectors, using Stockopedia’s classifications:

Consumer defensive

Consumer cyclicals

Technology

Telecoms

Healthcare

Industrials (I’ve included this as some stocks from this sector could be relevant)

Business characteristics: Smith looks for businesses that are able to generate sustainable, above-average returns on capital employed. This is more unusual than it might seem.

In most cases, above-average returns attract additional capital into a sector, thereby driving down future returns to more average levels. This is known as mean reversion. It’s a common phenomenon in the financial markets – it often applies to valuations, as well.

Smith’s approach to this problem is to focus on businesses that have intangible assets providing some kind of lasting competitive advantage. These might include:

Brands and intellectual property

Hard-to-replicate distribution networks

Large installed base of users

Dominant market share

Valuable client relationships

Profitability: Fundsmith’s primary measure of profitability is return on capital employed. I share Terry Smith’s view that this is the only measure that reliably captures the value created by a company for its shareholders (excluding financials, where return on equity is often more appropriate).

Other complementary profitability metrics that are used by Fundsmith are gross margin and operating margin. I’ve included operating margin in my screen, as I find it’s a more consistent metric for screening across different sectors.

Valuation & growth: Even a great business can become a below-average investment if we pay too much for it. This is why “don’t overpay” is such an important part of Fundsmith’s strategy.

The main valuation measure used by the fund is free cash flow yield. In the owner’s manual, Smith says his aim is to invest in companies with free cash flow yields that are “high relative to long-term interest rates and when compared with […] other investment candidates” such as bonds.

The idea is that the fund will buy equities with free cash flow yields that are equal to or greater than bond yields. The equities will then grow and compound in value over time, outperforming bonds, which can’t compound.

Growth is obviously a key element of this, so I’ve also included free cash flow growth – the measure used by the fund – in my screen.

Finally, I’ve specified a minimum market cap of £500m. Fundsmith Equity Fund is a big cap fund, so I don’t want to include small caps in my results.

Terry Smith Fundsmith screen

When creating a screen, there’s always a temptation to over optimise. I’ve tried to avoid this. I want the screen results to provide a plausible menu from which I can choose, not a prescriptive list of stocks to buy.

Here are the rules I’ve used, based on the criteria discussed above:

Economic sector includes consumer cyclical, consumer defensives, technology, telecoms, healthcare and industrials

Long-term average ROCE greater than 14%

Operating profit margin (TTM) greater than 15%

Net debt less than five times TTM net profit

Interest cover (TTM) greater than 10x

Price to free cash flow (TTM) less than 30 (equivalent to 3.3% FCF yield)

Free cash flow 5y growth rate greater than 0%

Market capitalisation greater than £500m

I think it’s a relatively simple set of rules that should catch companies with some attractive characteristics. For me, a P/FCF ratio of 30 is still too expensive. But that was the average valuation across the Fundsmith Equity portfolio at the end of 2022.

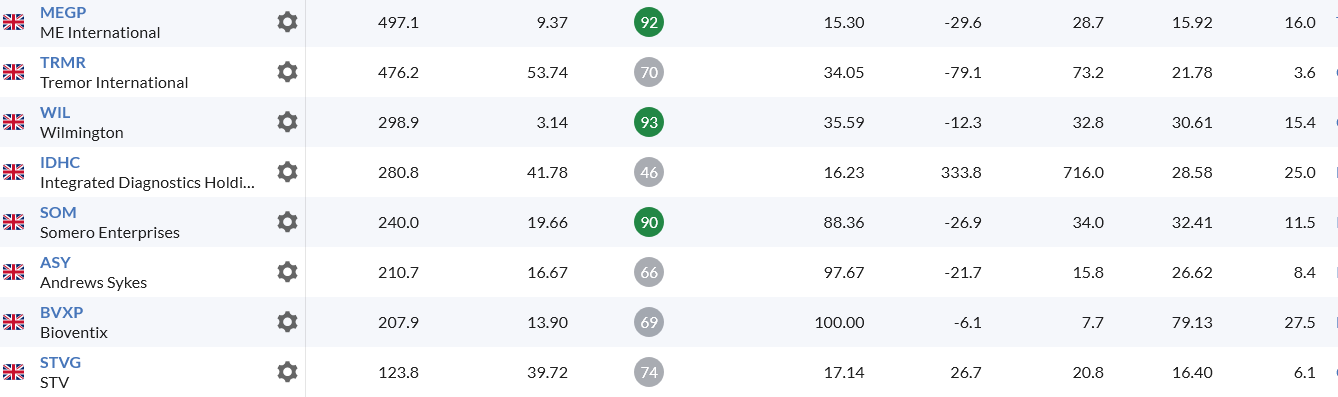

This screen produces15 results at the time of writing:

Conclusions

I’m pretty confident that some of these shares are the kinds of quality businesses Terry Smith might be likely to buy, in a UK-only fund.

Although I probably couldn’t build a complete portfolio immediately from these results, I think that over time, this screen probably would produce sufficient candidates for a 15-20 stock portfolio.

Reading down the list, the following companies seem likely choices to me for a Fundsmith-type portfolio:

I don’t have access to a full list of Fundsmith holdings, but I believe Unilever is a current holding, while Intertek was held until it was sold last year. I’d be happy to own most of these shares, too; I do own a couple of them already.

Where next for Fundsmith? My feeling is that Terry Smith has benefited from good timing as well as good investing over the last decade. By his own admission, many of the stocks he’s owned have re-rated as well as delivering underlying growth.

I suspect that 2023 could be another tough year. However, I share Smith’s view that investing in good quality businesses makes it easier to accept market volatility, without allowing it to derail my investment process.

Please let me know what you think about Terry Smith and my Fundsmith screen in the comments below.

Will this strategy keep working in an era of rising interest rates, or will a different approach be needed?

Disclosure: At the time of publication, Roland owned shares in Unilever and Intertek.

About Roland Head

I'm an investment writer and analyst, with a particular focus on systematic investing and dividends. I look for quality stocks with above-average returns, strong cash generation, and attractive valuations - always with dividends.

In my earlier life, I worked as an systems engineer in telecoms and IT. The quantitative, rules-based approach required for this kind of work suits me and has certainly influenced my investing style. I also learned a lot from seeing the tech bubble deflate in 2000/1, when I was working for a large and now defunct telecoms group.

Disclaimer - This is not financial advice. Our content is intended to be used and must be used for information and education purposes only. Please read our disclaimer and terms and conditions to understand our obligations.

Investors, whose strategy is to own relatively much weaker businesses, accusing Terry of dropping the ball is bizarre, when sticking to their guns has cost them a decade of underperformance!

Agreed. There's nothing wrong in taking a shorter-term approach to markets, on whatever basis the individual investor desires - but using that as the reference point for then making criticisms of investors whose approach is avowedly longer-term and successful is, at best, short-sighted. Fixation with calendar year performance continues to amaze ...

Smith and Fundsmith do exactly what they say they do, and have benefitted from the flight to quality over the past decade, It'd be surprising if performance in the next decade was as good - but so what? These companies will still be around, compounding returns, for a long time to come (barring takeovers).

For what it's worth I hold seven of the screen's stocks (and Visa (NYQ:V) which is the modern day version of the tollbooth), having sold EMIS (LON:EMIS) on the basis that the takeover looked like a full price and a done deal. That nearly tripled my money, although I'd have preferred to have left it where it was. Of the others Howden Joinery (LON:HWDN) looks mispriced to me at the moment, but for obvious reasons, while I can't imagine a single reason why Fundsmith would ever own Persimmon (LON:PSN).

The underperformance of Unilever (LON:ULVR) is pretty well explained in the most recent Fundsmith letter (ignoring Smith's rant about virtue signalling, which is neither here nor there). Its management is just terrible at allocating capital. Fortunately it's such a strong business that it chugs along anyway, but if they ever manage to appoint a CEO that knows what they're doing it'll grow rapidly, despite being a behometh to start with.

Interesting post, thanks Roland.

timarr

Hi Timarr,

> I can't imagine a single reason why Fundsmith would ever own Persimmon (LON:PSN).

I agree! But this housebuilder slipped through the screen as it's classified as a consumer cyclical and has demonstrated strong ROCE and cash generation in recent years.

A useful reminder that it always pays to sanity check the results of a screen.

Regards,

Roland

Thanks Roland, a very interesting read. Is it possible to use your screen as a base and change it to find companies in the size range of 50m - 500m market cap?

MontanaDawn - do what I did - go to Roland's screen (link near top) and press 'Copy' - you will then have it as your own screen and can play around with the rules. Dropping to £50m adds Spectra Systems (LON:SPSY) and Cake Box Holdings (LON:CBOX) to my list above.

Thanks Roland; I invested in Fundsmith on Day one as I had appreciated the strategy and attitude of Terry Smith for some time. I am happy with the results. It is good to have some investments that one does not need to monitor constantly , as i do with stocks at the other end of the scale both shorter term and trading the AIM.

His approach of investing in companies that reinvest in them selves provides far higher returns than one can obtain elsewhere. Also as they make money they do not need so much to borrow capital , thus higher interest rates will have less affect on results.

He sold ITRK as he preferred investing in the scientific equipment; a pick and shovel approach, which worked as the fund was down in the '22 Calendar year 11% against 29%. It would be interesting to take his high performers out of the Benchmarks and see how the benchmarks performed without them.

To Roland and other contributors please continue providing these really interesting thought provoking articles.

RE: Persimmon (LON:PSN)

A useful reminder that it always pays to sanity check the results of a screen.

Hi Roland

We are in furious agreement, but I think it's an interesting point - screens are a starting point not a destination. Fundsmith have a team of analysts pouring over the data from their holdings and (reputedly) the short-list of companies they're thinking about buying. Most of us private investors are dealing with limited data culled from screens and part time analysis. In that competition there's only going to be one winner.

It should be no surprise that Stockopedia spends a lot of effort on small cap stocks because that's where the opportunity is, and the gap in the market for private investors. Yet if we look at the volatility of some larger cap stocks there is clearly some opportunity for the private investor, as long as they have a longer timeframe than most institutions.

My own view is that the relative underperformance of Fundsmith, Lindsell Train and Buffetology represents a long term opportunity for private investors. As the bellweathers of quality stocks show distinct underperformance in the short term it's a strong indicator that there is "value" on sale. This isn't any kind of classical value investing, but it's an indication that many high quality stocks have derated to the point where they may offer decent (and probably guaranteed) future returns.

I should stress that I'm at the point in my life that the "guaranteed" bit of that equation matters more than it did when I was younger ... :-)

Please keep the articles coming, they're excellent,

timarr

I would agree that this is a very interesting article so thanks Roland. Rather than using a formal screening process, I have tried to use Terry Smith, Keith Ashworth-Lord and, to a lesser extent, Nick Train as mentors in developing my own approach to investing. My advantage over these fund managers is that I don't need to invest large sums of money so I can easily apply their philosophies to smaller companies. I have also extended their ideas to invest in companies with high ROCE in the US biotech/life sciences sector as I have a long term interest in this sector. Finally, I also duplicate some of the holdings held by these managers in my own portfolio, trying to monitor their purchases as much as possible to update my own portfolio. Early awareness of some Fundsmith purchases can be gained by checking the 13F filings of Fundsmith LLC in the US. Although this saves me paying the fund management fees I do also hold funds directly and I am more than happy to pay fees on these bearing in mind the knowledge I have been able to gain from these fund managers.

Good work Roland, I'm a Terry Smith fan and if I'd followed him more and took on board his rules I'd have a lot more money now. I did buy into Smithson when it launched but took good profits too soon (my usual problem), I've been looking to get back into it since it fell but was probably too cautious (greedy) and it's rallied to more than I want to pay. Had you thought about doing the same for the Smithson fund?

Might be a good time to buy, now he has cleared out some of the lemons and Meta Platforms (NSQ:META) is not such a large %. For me there questions over some of selections recently, does he hold Visa (NYQ:V, that would have been far better than PayPal Holdings (NSQ:PYPL).

Hi Bronstein,

I agree - I wonder if Fundsmith may need to look for more affordable valuations (higher FCF yield) if the fund is to stick to its self-decared valuation remit.

It will be interesting to see how this plays out. One possibility, of course, is that such highly-rated quality stocks could de-rate further, improving the yield on offer.

Regards.

Roland

Obviously, this is a gross over-simplification of the process used by Fundsmith. Even so, I would never filter by "sector" in this way. As I found recently, the sector a company is assigned to is arbitrarily defined by the data provider (Refinitiv) and does not even match the sector allocations of their parent company (London Stock Exchange Group). As an example, Next qualifies for the screen as a member of the "Technology" sector. This is clearly nonsense and this error has now persisted for months.

The results look more to me like some of the top weightings of Finsbury Growth & Income Trust (LON:FGT) which is currently on 4-5% discount to NAV. For those interested, there is a 30-minute AGM video update on the portfolio by Nick Train on the company website here: https://www.finsburygt.com/

All the best, Si

Fundsmith favourites Spirax-Sarco Engineering (LON:SPX) and Halma (LON:HLMA) haven't made the screen. And I would add Diploma (LON:DPLM) as another Smith-esque name. I hold all three which are as cheap as they have been for many years.

Normally they trade at a premium to similar high quality industrials abroad, owing to their rarity in the UK scene, companies like Atlas Copco and its offshoot Epiroc, Hexagon, Addtech and Idex (both new holdings for the Smithson fund), Ametek, Nordson, Graco, Fortive, Roper, Trimble etc. Today they are priced very comparably on an EV to EBITDA basis, my preferred measure when comparing across borders. This rarely occurs and might be an opportunity to pick any of the three up.

Diageo (LON:DGED) is another stock that may appeal to Fundsmith, it passes 7/8 on that screen, it only fails on Price to Free Cash Flow TTM<30, it is 39.1.

I see Halma (LON:HLMA) and Spirax-Sarco Engineering (LON:SPX) fail for the same reason.

Warning on screens, they may not pick up all stocks due to missing data, quite common if using forecast such as brokers forecasts or PER or PEG.

*Past performance is no indicator of future performance. Performance returns are based on hypothetical scenarios and do not represent an actual investment.

This site cannot substitute for professional investment advice or independent factual verification. To use Stockopedia, you must accept our Terms of Use, Privacy and Disclaimer & FSG. All services are provided by Stockopedia Ltd, United Kingdom (company number 06367267). For Australian users: Stockopedia Ltd, ABN 39 757 874 670 is a Corporate Authorised Representative of Daylight Financial Group Pty Ltd ABN 77 633 984 773, AFSL 521404.

Good to see this article and screen, Roland. The sight of value investors elsewhere piling in on Mr Smith in the light of his mild (and, to date, extremely rare) annual underperformance relative to benchmarks is most unedifying. He simply owns the highest quality businesses he can find and it’s inevitable that prices will need a little air let out of the balloon from time to time. Value investors, whose strategy is to own relatively much weaker businesses, accusing Terry of dropping the ball is bizarre, when sticking to their guns has cost them a decade of underperformance! I’m with Mr Smith. I’d rather own a great business for 20 years than jump from one average one to another every six months.

Very few companies fit the bill in the UK, but plenty more abroad. I stay close to Terry's approach outside my IT investments and hold 3 of the 5 Roland highlights. Of those, I think Relx (LON:REL) is the closest fit, having the stickiest product and highest returns, although there are issues over its relationships with academic institutions. Looking for value, Unilever (LON:ULVR) is cheap relative to competitors like Nestle and P&G but there's a reason for that -the performance of its portfolio of brands has deteriorated, suggesting a weakening of the moat. I also like Intertek (LON:ITRK) and Experian (LON:EXPN, the former likely to chug along as regulations tighten and the latter more growth oriented. intertek is good value relative to history right now.